Autodesk Q4 FY1/26 Earnings Review. Is This The Bottom? (NO PAYWALL)

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Will Autodesk Be An AI Winner?

by Alex King, CEO, Cestrian Capital Research, Inc

If you missed our recent note on where we think software is headed, please take a moment to read it, here.

Enterprise software is going to divide very shortly into AI winners (companies that truly internalize and leverage AI tools) and losers (those that resist). Success, I think, comes down to these factors:

- Does the CEO recognize the tectonic shift happening in the industry and its immediacy, and;

- Is the CEO able to internalize what this means for their business and then turn that into a transformation plan?, and;

- Can the CEO then execute the transformation plan both in reality and also project the success of the plan to capital markets participants.

This is how life will be in software now. Many will fail.

Autodesk (ADSK) is aware of the problem and, if the company’s CFO is anyone to go by, is trying to internalize AI. Here’s what the CFO said at a Morgan Stanley conference on 4 March this year:

From the transcript.

Janesh Moorjani

Executive VP & Chief Financial Officer

Yes. We have been big users of various AI tools and technologies internally. When things first started to move, call it, a little over a year or so ago, we had 1,000 flowers bloom. We just encourage people to keep adopting it and using it in creative ways to see how they would actually be able to benefit from it in their day-to-day work. A lot of it was just basic productivity enhancements, but productivity enhancements, not in the form that you could immediately monetize. It made us – it helped us better prepare for our earnings call, but that doesn't translate into real dollars saved anywhere. So that's just one example. But on the development side, now we've started to do a lot more. We've rolled out Claude code quite widely within the organization.

Developers are a lot more productive. And the way I think about this is over the course of the long term, we're going to invest a certain amount of dollars into hiring additional engineering capacity, hiring headcount. And what this allows us to do is shift some of those headcount dollars to technology dollars. We don't want to use AI to limit the output of the organization and drive cost savings. But the way we're thinking about this is if we can use it to drive greater velocity and greater productivity in the development organization while staying invested in R&D, it will just help us accelerate that much faster, and it will help pull the future into the present that much faster. So we're using it as a way in which we can drive greater productivity. And in the initial stages, that also means a greater level of investment on the part of the company because we want to drive the adoption so people see the benefits and don't let the cost be a reason not to adopt the technology in the early stages.

“Greater productivity” = more revenue/head as a simple proxy. So it’s possible that ADSK sees rising margins as a result of adopting AI tools. As I’ve highlighted often, there is a double benefit to less heads in a software company - the first is higher net income, because less staff cash costs; the second is fewer shares created, because lower stock-based comp; combine these facts and it may deliver a material step up in earnings per share, on the basis of earnings up and shares down (or at least shares not up by as much).

Autodesk Stock Chart

The ADSK chart is one to watch for a sign of bottoming.

Support has held at $214 for about two months now. If it breaks that makes a lot more downside likely of course; if it holds, then the low may be in. Software has, as you know, been under a lot of pressure lately so if ADSK can hold around here, that’s a bullish look.

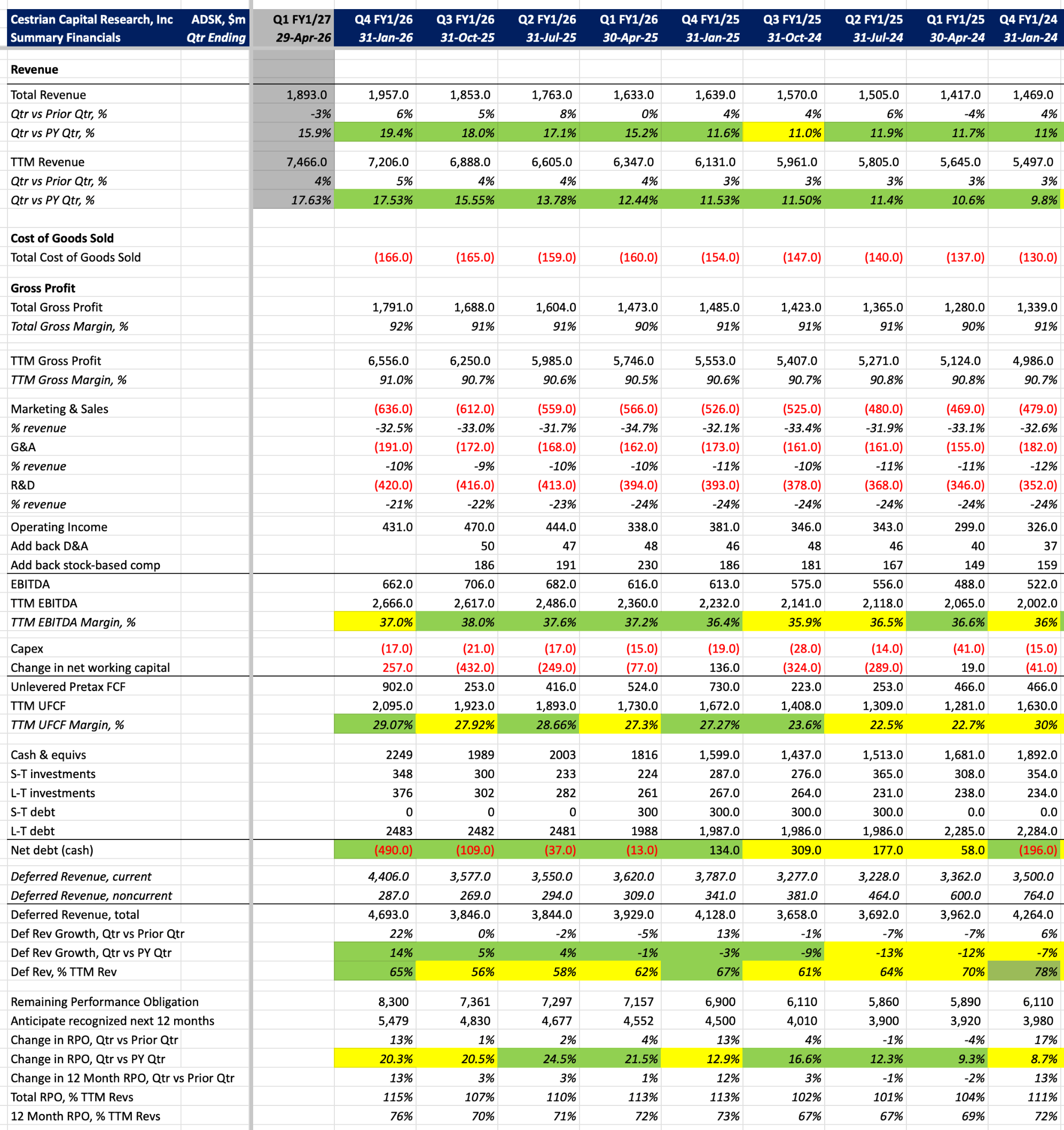

Autodesk Fundamentals

The rate of growth of RPO (the order book) has outpaced growth in recognized revenue for some quarters now, but the gap is closing. It’s no surprise therefore that the company is guiding that growth next quarter will cool off.

Cashflow margins remain very strong and the balance sheet is improving, now with $500m of net cash.

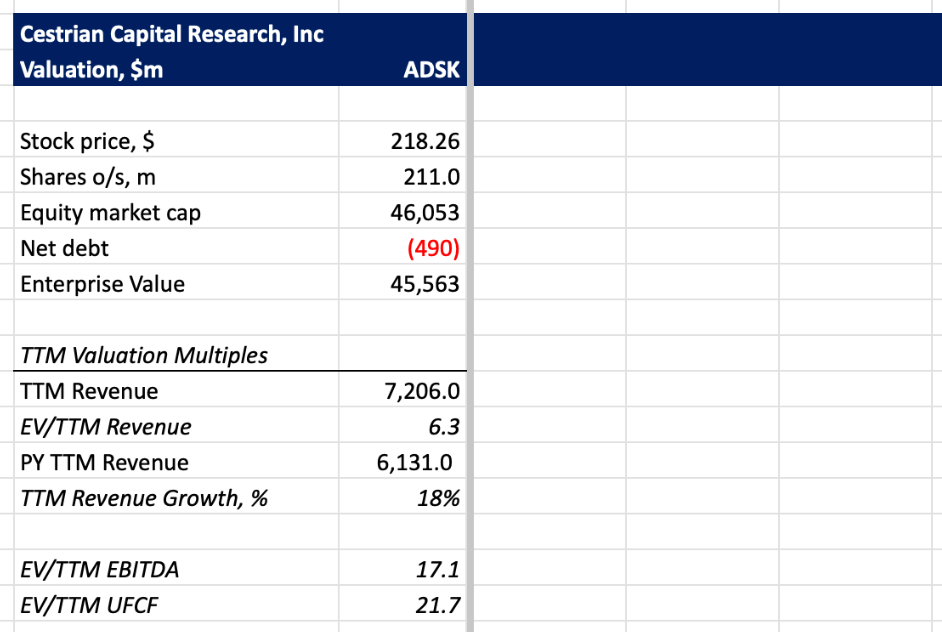

Autodesk Valuation

The reason software has been beaten up so badly is that even after the beating has been admonished, valuations remain punchy!

Stock Rating

We may be at a sector low in software right now but a big one-way bet on that would be foolish. I think ADSK can be accumulated at present with a tight-ish stop below the current support level. 2026 calendar Q1 earnings for software stocks will be critical, not just the numbers but also the story.

Cestrian Capital Research, Inc - 11 April 2026

Learn more about Cestrian Circle, here.