Bonds Are Toxic.

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Analysis by Alex King, CEO, Cestrian Capital Research, Inc. + Claude CoWork.

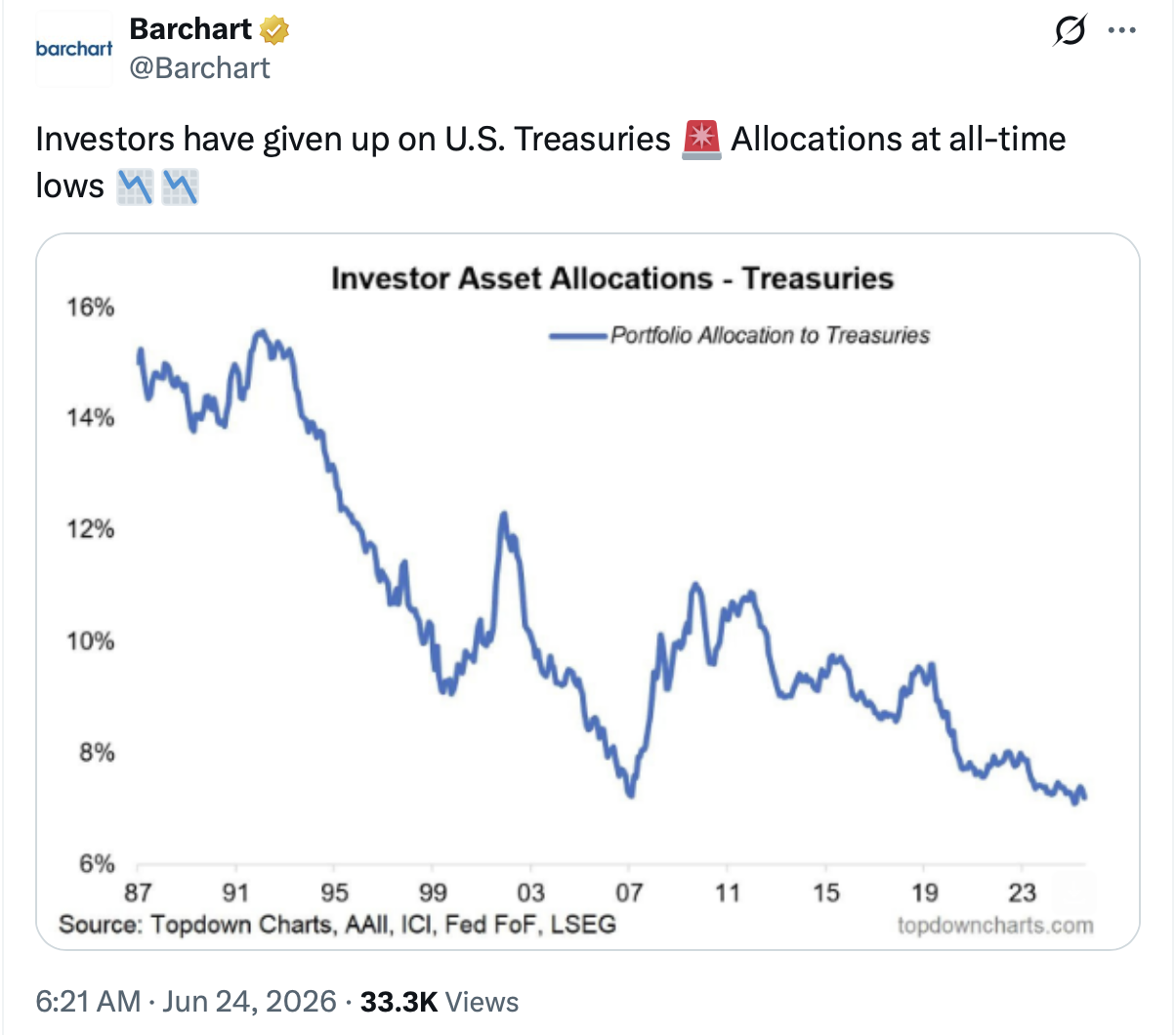

Analysis was posted today by Barchart stating that investor allocations to US Treasuries are at all-time lows.

I thought this was pretty interesting, not least because I think rates are going to fall and bond prices rise, and because our SignalFlow For Bonds service has also been kicking into gear lately. (SignalFlow Bonds is one of our quantitative algo services. It helps you trade bond ETFs like $TLT and others to good effect. You can read about it here and here).

First of all, is this true? Have investors deserted U.S. Treasuries?

The Headline Is Wrong, The Direction Is Right

As one of my former colleagues used to say, the Barchart attention-grabber is, er, “directionally correct”. (It amused me no end to see that Claude reached that exact conclusion in its analysis!).

Taken literally, "all-time low allocations to Treasuries" is false. In dollar terms, the world owns more Treasuries than it has ever owned in history — it has to, because there are more of them than ever. Publicly held federal debt has gone from around $6.4 trillion in 2008 to roughly $31.4 trillion by April 2026. So somebody is holding all of that paper. Absolute allocations are at record highs, not record lows.

But the claim is directionally correct if you measure the right thing. Through the lens of the share of portfolios, there is truth to the argument.

- Foreign ownership share is at a multi-decade low. Overseas investors hold around $9.5 trillion of Treasuries — about 30% of publicly held debt, down from nearly 50% in the early 2010s. Contrary to the “overseas holders are dumping Treasuries” line you see all over FinTwit, such investors have in fact kept buying, just not in sufficient quantities to keep pace with issuance.

- Fund managers are persistently underweight. Bank of America's June 2026 Global Fund Manager Survey had a net 42% of managers underweight bonds, broadly in line with 44% in May.

- The reliable institutional buyers are stepping back. The Fed is running down its balance sheet rather than adding. Corporate defined-benefit pensions — long the natural home for such securities — are now around 108% funded, have largely completed their de-risking, and have eased off bond buying.

Why Investors Are Staying Away

The logic for underallocation has included:

Relentless Supply

The federal deficit is running at roughly $1.9 trillion, or about 5.8% of GDP — a peacetime, full-employment deficit of a size that used to be reserved for recessions and wars. Debt held by the public is around 101% of GDP and the Congressional Budget Office has it climbing toward 120% by 2036, which would pass the post-WWII record if it actually happened. (We should all note that such forecasts are rarely accurate).

Term Premium Has Been Climbing

For most of the 2010s, investors demanded almost no extra compensation to lock up money for ten or thirty years instead of rolling T-bills. That term premium is now rising again — still below its long-run average, but until recently has been heading the wrong way for bondholders. A rising term premium pushes long yields up independently of what the Fed does, which is exactly why the 30-year topped 5.19% in May 2026, its highest since before the financial crisis, even as shorter-term yields stayed anchored.

The Market Believes The Fed May Hike

The market believes that inflation is proving sticky and therefore stagflation bets have been rising. Markets have been pricing roughly even odds of a September hike. The recent rate hike by the ECB has been used as supporting evidence for this narrative.

So Now … The Bull Case For Bonds

Since the dominant narrative is negative, it is probably wrong. Personally I think the ECB made a policy mistake, hiking due to short-term supply side factors (the inflationary impulse from the Gulf war), and will soon have to reverse course. The Bank of England has cut; I think the Fed will cut this year. This is just my opinion of course. Let’s see if there is any supportive evidence for wanting to own U.S. Treasuries at this time.

Yields Are Now Meaningful

The 10-year sits around 4.45%, the 2-year around 4.2%, and the 30yr above 5%. Those are the best entry yields in roughly two decades, and with inflation in the low-to-mid 3s, the real yield is positive and meaningful. You are now paid a genuine carry simply to hold the asset and wait. Bonds at 5% are a fundamentally different proposition from bonds at 1.5%. That argument gets stronger should inflation actually start to fall.

Belief Is Absent

A net 42% underweight in bonds is not a starting gun, but it tells you the marginal seller is largely spent and the pain trade is a rally, not a sell-off.

If The Economy Weakens, Bonds Can Protect A Portfolio

It is unclear to me whether the US economy is weakening or not. The capex-fueled growth looks like it can stay awhile to me. But if we do get a consumer slowdown, Treasuries should benefit, and buying that insurance at a current 4.5-5% yield doesn’t seem foolish.

A Selection Of Bond ETFs

Not everyone wants to hold bonds directly; for those interested in holding bonds via ETFs, we cover $TLT, $SHY, $IEF and $ZROZ. These ETFs are correlated to some degree but are not four versions of the same bet. They sit at four different points on the curve, with four different durations, and each one is a lever on a different scenario. Duration is the key number — roughly the percentage price move for a 1% change in yield.

$SHY — iShares 1–3 Year Treasury (duration ~1.9 years)

This is the cash-substitute. With a duration under two years, its price barely moves; almost all of your return is the yield itself. SHY appreciates meaningfully only if the front end (short-term yield) falls — i.e. the Fed actually cuts. In today's setup, where the market believes the Fed is flirting with a hike, that's the lever the market thinks is least likely to fire near-term. SHY can be used to harvest 4%+ yield with minimal price risk, or as a parking spot for cash.

$IEF — iShares 7–10 Year Treasury (duration ~7 years)

With ~7 years of duration, IEF offers some capital-gain potential if yields fall, without the full fiscal-risk exposure of the very long end. It is the cleanest expression of a "growth slows, inflation cools, Fed eases modestly” view.

$TLT — iShares 20+ Year Treasury (duration ~16.5 years)

The long bond, and the headline duration play. At ~16.5 years of duration, a 1% fall in long yields is worth roughly a 16–17% price gain — and the same in reverse. TLT needs the long end to rally: a genuine recession, a deflation scare, term-premium compression, the return of foreign or Fed buying, or a flight to quality. It is the highest-conviction bet on "long rates are going down." But it is also the most exposed to the bear thesis above — a bear steepener driven by fiscal worry or a hot inflation print hits TLT hard.

You can open a full page version of this chart, here.

$ZROZ — PIMCO 25+ Year Zero Coupon STRIPS (duration ~27 years)

This is the most aggressive Treasury vehicle in the listed universe. ZROZ holds zero-coupon STRIPS — the stripped principal payments of Treasuries with 25+ years to maturity — which means no coupons, maximum duration, and maximum convexity. Effective duration sits around 27 years, so it behaves like a turbocharged TLT: in a sharp long-end rally it will outrun every other fund on this list, and in a sell-off it will fall the furthest and fastest. ZROZ only makes sense if you have genuine conviction in a decisive collapse in long yields — a hard-landing, rate-shock, "the Fed has to slam the brakes the other way" scenario. Its convexity is a gift when you're right and a wrecking ball when you're wrong. You probably want to size it accordingly.

Cestrian Capital Research, Inc - 24 June 2026

DISCLOSURE: Cestrian Capital Research, Inc staff personal accounts hold long position(s) in $TLT.