Cloudflare (NET) Q1 FY12/26 Earnings Review

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Fit. Getting Fitter.

By Hermit Warrior a.k.a. Richard Iacuelli

...roles are changing dramatically, and you've got to do something dramatic in order to make that shift, and that's why this was the right time. In other words, we're the fittest we've ever been, but we're going to get even fitter to win the next chapter.

Matthew Prince, Co-Founder & CEO, Cloudflare

House View

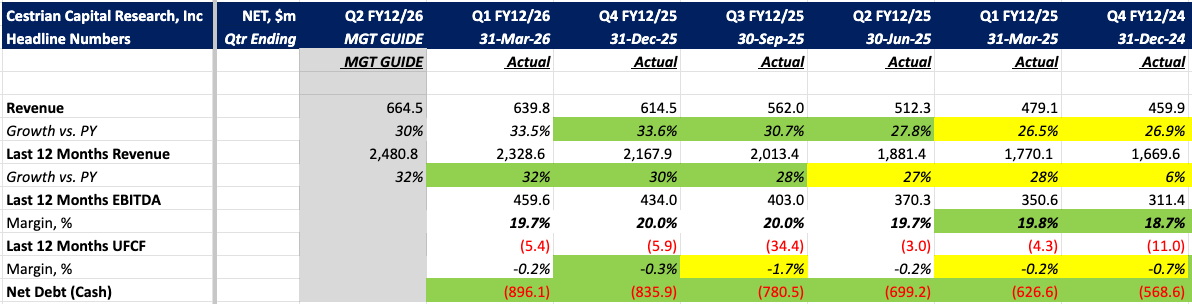

Strong quarter, ugly reaction. Cloudflare's ($NET) Q1 revenue of $639.8M grew 34% year on year — matching Q4's growth rate and clearing the 30% guide — with $1M+ deals up 73%, the fastest growth in that cohort since 2024. The stock however fell ~25% over the next few sessions, with the workforce restructuring announced with earnings (more than 1,100 roles to be cut, approximately 20% of the workforce) potentially a catalyst.

The market's scepticism wasn't wholly unwarranted. Underneath the solid headline growth rate, several key metrics plateaued or went in the wrong direction. Q1 revenue growth 'only' matched growth in Q4 after three sequential quarters of acceleration; total RPO growth decelerated from 48% in Q4 to 36% in Q1; GAAP Gross margin compressed to 71.2%, down from 73.6% in Q4 and 75.9% a year ago, with the fast-growing developer platform carrying lower margins. Plus, the Q2 guide of 30% growth is again lower than the revenue growth achieved in the last two quarters.

That said, there were strong positive counterpoints to balance out the negatives: More customers spending $5M+ annually were added in Q1 than in the whole of 2025; a surge of free accounts shifted to paid (contributing to those lower gross margins as the cost of free services shifted from the 'sales and marketing' expense line, to 'cost of goods sold'); bookings from new customers increased at the highest rate since 2023; and the sales pipeline in Q1 increased sequentially at the fastest rate since 2021.

Further, CEO Matthew Prince framed the cut roles as transformation, not retrenchment - rebuilding the organisation around what Prince called 'an agentic AI-first operating model' - with quota-carrying salesforce preserved, FCF guidance unchanged, and internal AI usage driving exponential productivity gains turning proof of concepts into "core parts of our workforce" as the company goes from fit, to fitter.

The strategic thesis — Cloudflare as the infrastructure layer of the Agentic Internet — remains intact. A subsequent recovery in the stock price to new all time highs, less than a month after earnings, points to investors staying faithful to the vision, for now.

Here are the headline numbers.