CrowdStrike (CRWD) Q4 FY1/26 Earnings Review

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Setting a High Bar

By Hermit Warrior a.k.a. Richard Iacuelli

Here's what you have to remember, it's that what customers want is real-time prevention. You have to be in line. You have to be able to get the data in milliseconds, and you have to make a decision. That's not the case with an LLM. There's many great things it can do, and it's certainly a fantastic technology, but it's not stopping any breaches in real time. And that's one of the areas, I think, again, where we shine.

George Kurtz, Founder & CEO, CrowdStrike

House View

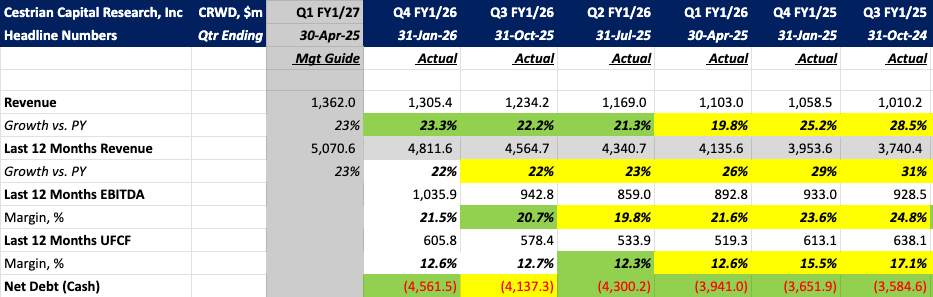

A very good Q4 for CrowdStrike (CRWD) which joined only Cloudflare (NET) - for the cybersecurity names we track - in seeing accelerated revenue growth for a third consecutive quarter. 23.3% revenue growth year on year beat the 22% guide by a respectable margin, with management guiding for 23% growth in Q1 - which they will also likely beat, resulting in potentially a fourth consecutive quarter of accelerating revenue growth.

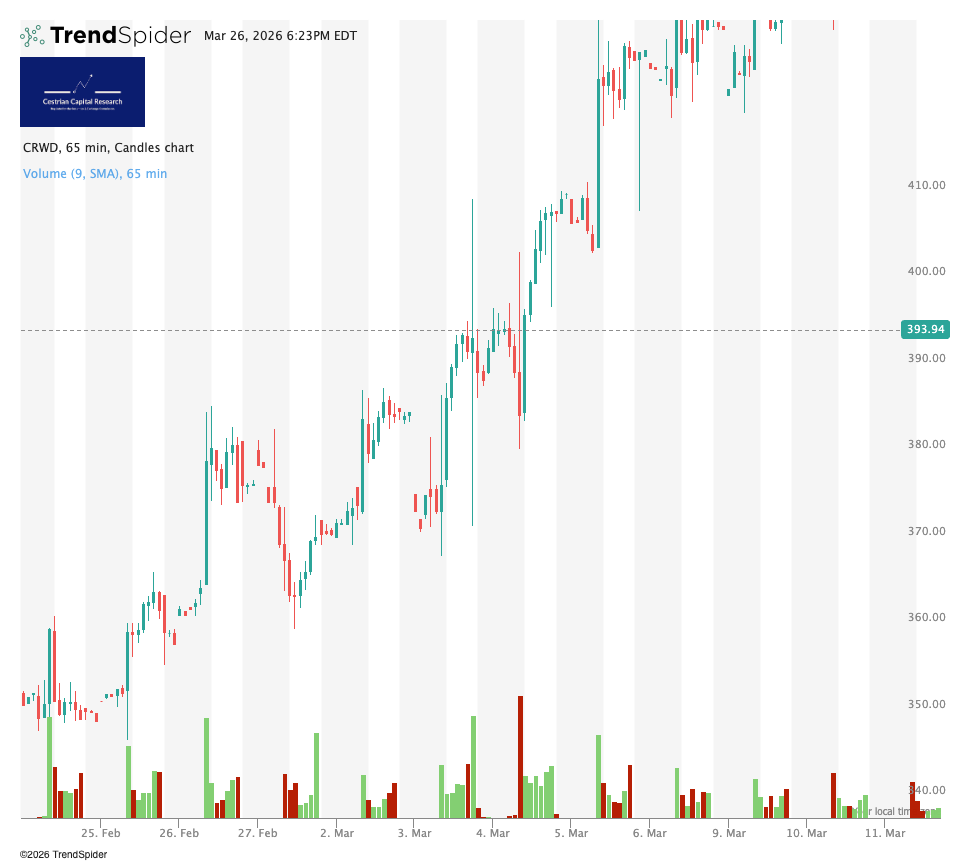

As is its wont, the market took it in turns to shrug, freak out, and finally send the stock ripping higher in subsequent days. That doji candle in the middle of the 65 minute chart marks the stock's performance in the hour of the earnings release - big up and down swings but little movement in the end. The dotted line by the way is where the stock closed yesterday, three weeks later - again basically going nowhere.

A standout metric was the 47% year on year growth in net new ARR (annual recurring revenue) - another third consecutive quarter of acceleration - and a number that puts Zscaler's (ZS) organic net new ARR growth of 7% in Q2 FY26 into (shaded) perspective. A stated target of $20B ARR by FY2036 target is ambitious — a near-quadrupling from today's $5.25B, roughly 14% compounding growth over a decade - but not unreasonable given the current trajectory.

CEO George Kurtz joined peer Nikesh Arora from Palo Alto Networks (PANW) in addressing the 'AI eats software' narrative, spending considerable time in his prepared remarks and mounting a full-throated counter-argument: that AI divides software companies into two groups, those that are existentially threatened (nice-to-have, point products, legacy pricing models) and those that will thrive (mission-critical infrastructure, proprietary data, trusted architecture). CrowdStrike, in Kurtz's telling, is firmly in the second camp.

Here are the headlines.