DataDog Q1 FY12/26 Earnings Review (No Paywall)

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Beware Gravity

by Alex King, CEO, Cestrian Capital Research, Inc

The “software is dead” crowd is likely to take a beating in the near future, at least if the technical setup in the sector ETF $IGV is anything to go by.

Heavy accumulation between $76-$88/share looks like it is being rewarded by a move into the markup phase - even if the 200-day moving average at $100 caps it for a time, that is still up to 30% gains from the recent lows for anyone doing their own work rather than following the narrative.

I think the AI-kills-software thesis will turn out to be, mostly, bunk. The best software names will use agentic capability to hollow out their headcount and replace it with automation. The benefit should flow to cashflow (lower cash comp if you have less humans) and in particular to EPS (because you don’t have to pay machines anything in stock, so stock-based-comp should fall faster than operating expenses - meaning net income should grow faster than cashflow, and since there will be less shares issued, the denominator of earnings/share should rise less quickly too … so, more earnings, fewer shares, more EPS, all other things being equal.

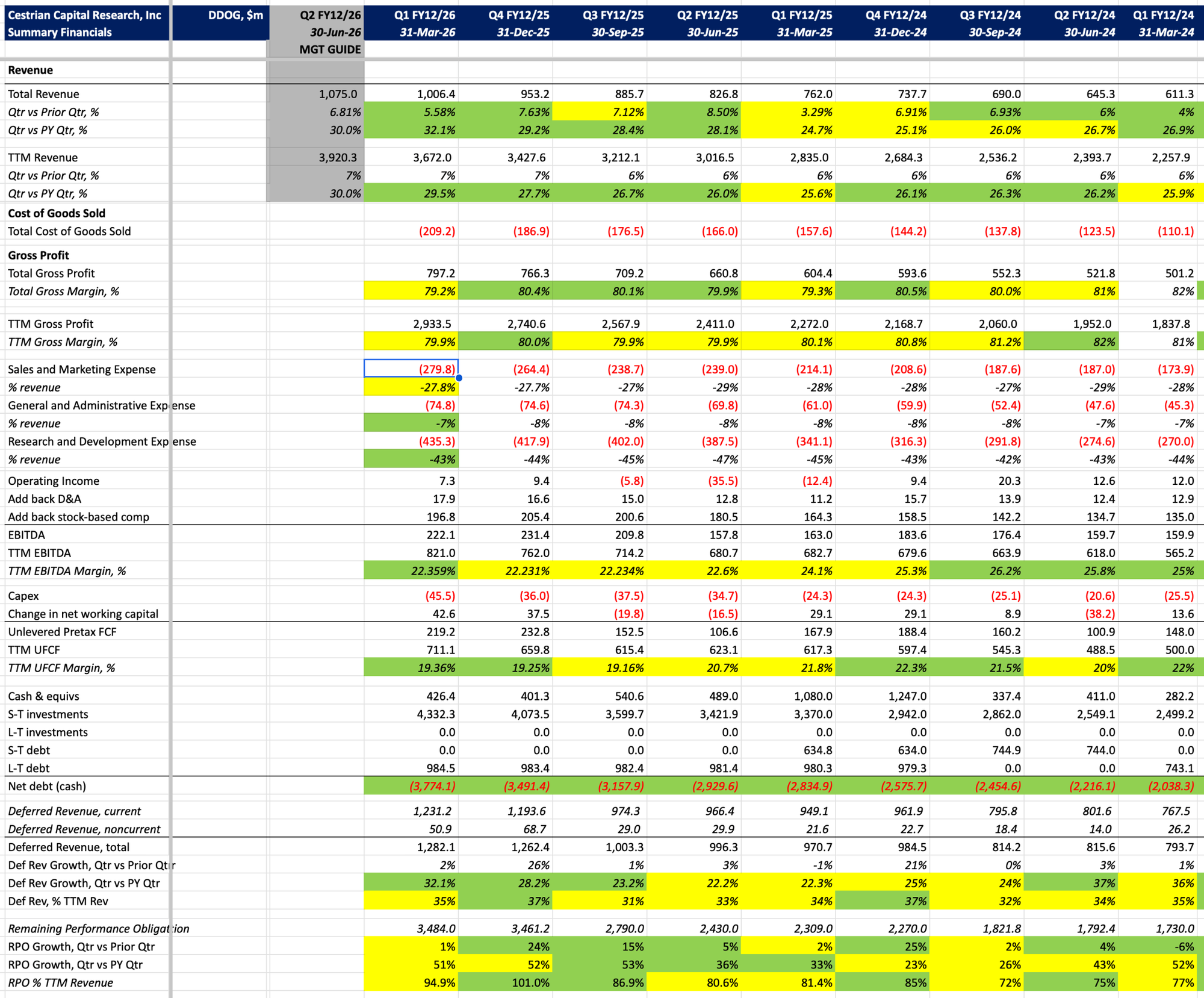

Now, $DDOG has the opportunity to do this, since it issues a huge great whacking slug of stock-based comp each year - in the last twelve months, SBC has been $783MM, a little more than the total unlevered pretax free cashflow generated in that period. Those TTM UFCF margins are also under 20%; if the company chose to get really efficient with automation, we could see TTM UFCF margins closer to 30% as well as the stock-based comp bill - and therefore rate of dilution - coming down.

The stock mooned on earnings; this was due to a very strong revenue performance. Growth ticked up to +32% for the quarter vs. the same quarter last year, and +29.5% on a TTM basis vs. this time last year. The guide also indicated 30% growth qtr vs. prior year qtr, materially higher than has recently been the case.

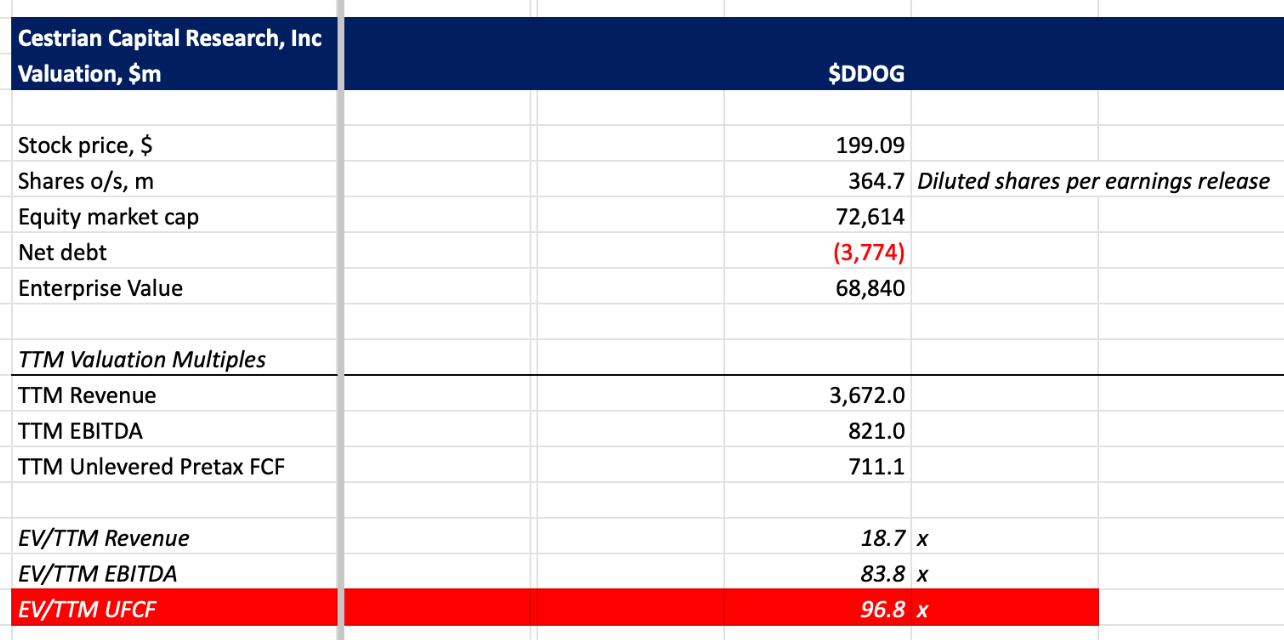

The order book - RPO - saw a rapid slowing in growth. That is a red flag until proven otherwise. And the valuation multiples right now are, shall we say, elevated.

The chart looks a little precarious up here - I think the stock can go higher for sure but if I owned this one I would probably want a stop in place a little below the opening price post earnings - just to keep me safe if there is a gap fill.

We rate the stock at Hold, assuming you have some kind of risk management method in place.

Cestrian Capital Research, Inc - 12 May 2026

Start Your 30-Day Free Trial Of Cestrian Circle

We are opening up a limited-time 30-day free trial for Cestrian Circle, Cestrian’s introductory research tier and the easiest way to start using Cestrian’s research regularly at a lower commitment level than Inner Circle.

Circle is built for investors who want a simpler way to stay close to markets, earnings, and trade setups.

Members receive twice-weekly research selected from trade roundups, earnings coverage, and sector reports.

Enter billing info to activate the trial, pay nothing today, and cancel before the 30 days end if Circle is not for you. If you stay, membership continues automatically at $39/month.