Is A Short Squeeze Setting Up In Oil? (NO PAYWALL)

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Analysis by Alex King, CEO, Cestrian Capital Research, Inc + Claude CoWork

As everybody knows, nothing about securities prices should be suprising in relation to IRL. Two edge cases to prove a point. Remember this one from the Covid crisis?

And now we have this:

As US efforts to achieve a cessation of hostilities and an opening of the Strait have continued, short oil positioning has climbed - with great success thus far, contrary to the narrative or expected “what should happen” as regards oil prices.

As a result of this unexpected win for shorts, every tourist oil analyst including myself is asking: is a short squeeze setting in? In my case, having no oil expertise whatsoever, my interest is not because of anything to do with IRL - I doubt the world is about to run out of oil - but purely due to extreme onesided positioning in this trade.

Short squeezes, when they happen, can be free money on the long side if you catch them right. So is there an opportunity to do so?

Let’s dig in to this question.

The Short Side Is Crowded

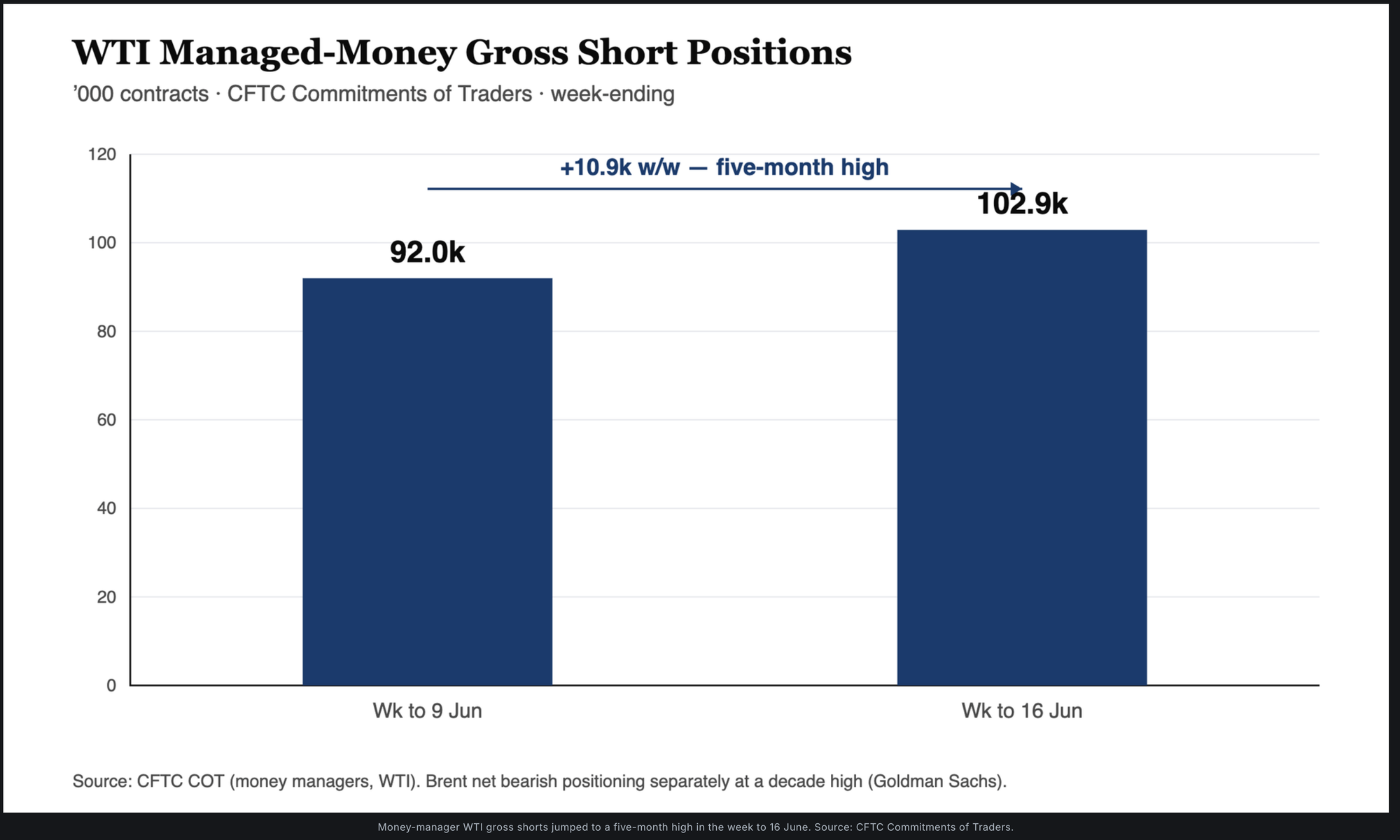

Let’s start with the Commitments of Traders data. Reported positioning has become stretched and one-sided.

In WTI, managed-money short positions pushed to roughly 103,000 contracts in the week to 16 June — a five-month high — with money managers adding around 10,900 gross shorts in that single week. In Brent the picture is more extreme still. Goldman Sachs' futures desk flagged roughly $24.8bn of selling over a seven-week liquidation wave, of which about 80% came from new outright short positions rather than longs being trimmed. That has driven bearish Brent positioning to its highest level in a decade.

Why does this matter? Because - remember - a squeeze is a mechanical event, not a sentimental or fundamental one. When a large, lop-sided population of traders is short and the price starts to move against them, they are forced to buy to cover — and that forced buying pushes the price higher, which trips stop-losses and forces still more buying. The more crowded the short, the more combustible the setup. Right now the short side is about as crowded as it gets.

The Physical Market Tells A Different Story

Here is the tension with the real world.

The recent slide — Brent back to around $77–79 and WTI near $73–74 as of 22 June — was a positioning washout driven by hopes of a US–Iran de-escalation, the prospect of Iranian barrels returning, and easing fears around the Strait of Hormuz. Underneath the selloff, the physical market is still behaving like it is tight:

- The curve is backwardated. Front-month barrels are priced above deferred contracts — the market's way of saying prompt supply is scarce and buyers will pay up for oil now rather than later.

- Inventories are below normal. The EIA's weekly report showed a 7.2 million-barrel draw, leaving commercial crude stocks around 426.5 million barrels — roughly 5% below the five-year seasonal average. Stocks are being pulled down, not built up.

- Supply is being held back. OPEC+ continues to keep a tight rein on output, and the EIA's own Short-Term Energy Outlook models sizeable global inventory draws through Q2, with a Brent forecast sitting well above where futures currently trade.

So the paper market is positioned for a surplus that the barrels are not yet showing. One cannot say whether paper or physical worlds are correct; one can just observe the difference and try to trade accordingly (with risk management methods in case wrong).

What Could Light The Short-Squeeze Fuse?

A setup needs a catalyst. For this one, the trigger would be anything that makes the crowded bearish trade look wrong, forcing shorts to cover into a thin, backwardated market - including but not limited to:

- A US–Iran deal that disappoints on the volume of barrels it actually frees up.

- A fresh geopolitical flare-up impacting oil supply.

- A surprise inventory draw, or OPEC+ holding the line on supply for longer than the market assumes.

Price > Opinion

As always price is correct and opinion is irrelevant. Short squeezes are relatively rare at scale. Extreme short positioning has no clock attached to it, the same as extreme long positioning. If you tried to short the semiconductor rally you will know this. Positioning can stay crowded for a long time.

Second, the shorts may simply be right. If a peace agreement holds, Iranian exports ramp meaningfully, and global demand softens into a slowing economy, the bearish thesis pays off and there is no squeeze — just a market that correctly anticipated more supply. Record short positioning can reflect a genuine, well-reasoned expectation of surplus, not merely a herd.

So What?

The net of it: this is a coiled spring. There is have a near-record short base in WTI and a decade-extreme one in Brent, set against a backwardated curve and below-average inventories — the cleanest squeeze setup the oil market has offered in months. What is missing is the trigger, and triggers are by nature unpredictable. So I am not arguing for a rip in oil prices right now; I am flagging that the conditions for a sharp, mechanical move higher are unusually well aligned, and that anyone positioned short here is playing with a crowded exit.

Cestrian Capital Research, Inc — 25 June 2026

DISCLOSURE: I am long $USO and a basket of energy stocks that probably benefit from rising oil prices.