Is Marvell Technologies The Next Micron? (NO PAYWALL).

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Q4 FY1/26 Earnings Review And More

by Alex King, CEO, Cestrian Capital Research, Inc with help from Claude and Gemini.

The game in datacenter component investing thus far in the AI boom has been (i) have a working knowledge of the internal structure of the hyperscalers’ datacenters (ii) understand which pinch point is currently being relieved with new product - the better to avoid major market tops when late buyers show up - and (iii) understand where the next pain point is & try to invest in that. This is why the money has been rolling from GPU stock(s) to DRAM stocks to photonics &c. Marvell, I think, has the opportunity to be a future big winner as everyone piles in. (The equity market does have to be supportive, of course; continued weakness in technology names will drag down all such names.)

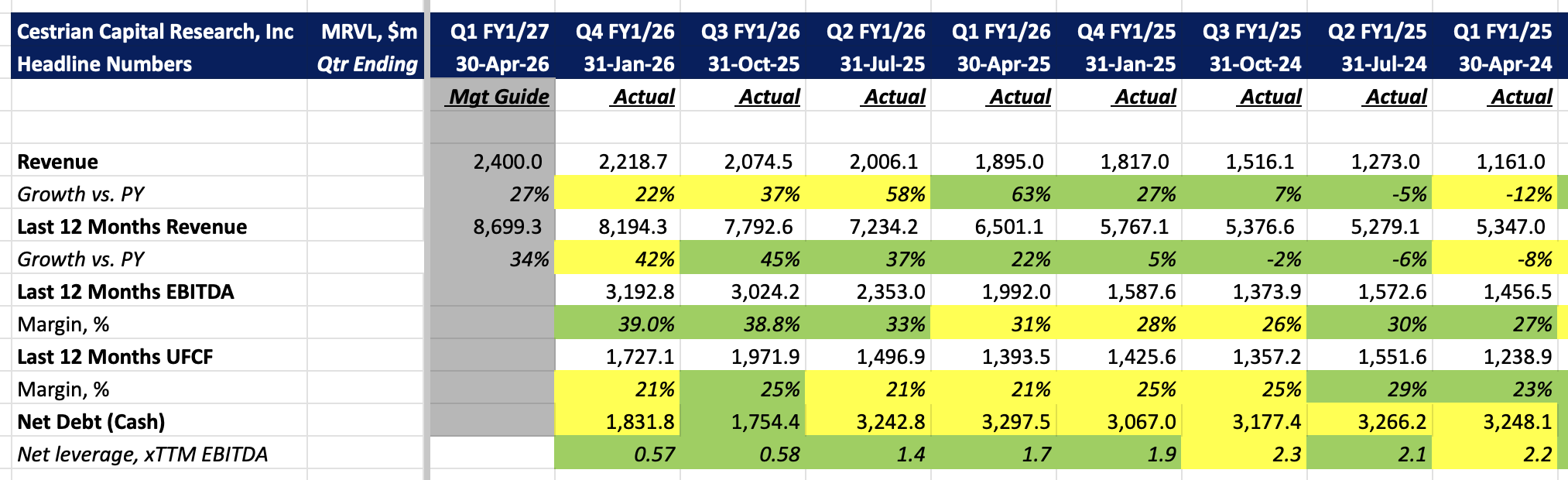

Financial Fundamentals

Here’s the headlines. Growth slowed to +22% vs PY this quarter, but the company is guiding for an acceleration to +27% next quarter. Cashflow margins took a hit but are fine at +21% on a TTM basis. And the balance sheet is very lightly levered, less than 1x TTM EBITDA.

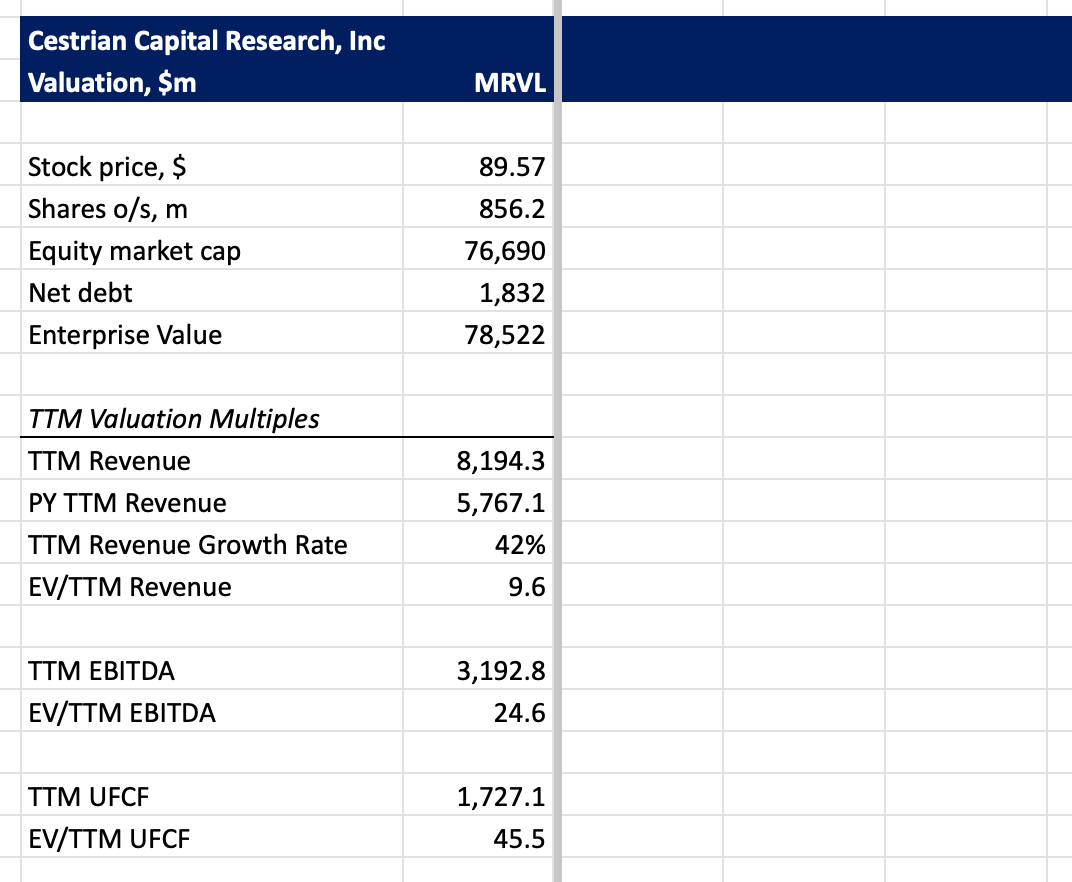

Valuation

Not cheap. 45x TTM unlevered pretax FCF for 27% growth as guided.

Before we take a look at the stock chart, let’s now consider the Bull (Marvell is special) vs Bear (it isn’t) take on product set and opportunity. Ultimately stock price is primary but here’s how we assess the unders and overs of this company.

Inner Circle members only - if you want to get into the weeds on the detail here, please feel free in Slack Chat - we have many semiconductor industry experts in our community who are always happy to help.

The Bull Case

Marvell has positioned itself as a critical infrastructure supplier for AI datacenter buildouts, addressing multiple structural bottlenecks simultaneously. Its optical DSP chips (Orion/Canopus) dominate the 400G/800G transceiver market in a near-duopoly with Broadcom, and at the emerging 1.6T tier Marvell currently faces no production-ready competition — an effective monopoly window of 12–24 months. Its Brightlane CXL memory controller IP addresses the memory bandwidth bottleneck relevant to large-scale inference, while its Teralynx Ethernet switch ASICs serve AI cluster networking.

The most strategically significant element is the custom ASIC business. Only Broadcom and Marvell can deliver hyperscaler-specific AI accelerators at production scale on leading-edge nodes (TSMC N3/N2). Once a hyperscaler has co-developed a custom chip with Marvell over a 2–3 year cycle, switching costs are prohibitive — creating per-customer quasi-monopolies with Google, Amazon, Meta, and Microsoft. Longer term, early Co-Packaged Optics (CPO) development positions Marvell as a potential first-mover in next-generation switch connectivity, expected to become critical at the 3.2T tier around 2026–2028.

Financially, the transformation is well advanced: as noted above, FY2026 revenue reached $8.2bn, up 42% year-on-year, with datacenter representing approximately 74% of total revenue. Despite this, Marvell trades at a meaningful discount to Broadcom on forward multiples. The bull view holds that the market recognises Marvell as an AI beneficiary but undervalues the depth of its moat — particularly the captive nature of hyperscaler ASIC relationships, the 1.6T DSP timing advantage, and CPO positioning.

The Counterpoint

The bear case centers on several structural concerns. Concentration risk is significant: dependency on a small number of hyperscalers means a single customer’s architectural pivot or insourcing decision could remove a large, non-replaceable revenue stream. The very depth of engagement that provides stability also amplifies the downside of any customer defection.

The 1.6T DSP monopoly window may prove shorter than expected. Broadcom has historically moved quickly to close product gaps, and any earlier-than-expected breakthrough from Credo Semiconductor would compress margins materially. The valuation discount to Broadcom may also be structurally justified rather than a perception gap: Broadcom’s diversification across software, enterprise, and infrastructure provides earnings resilience that Marvell — now a high-beta AI capex cycle play — lacks.

On custom ASICs, revenue growth is partially offset by margin dynamics: hyperscalers hold significant pricing leverage in co-development arrangements, making ASIC gross margins likely lower than merchant DSP silicon. CPO remains pre-revenue at scale and risks being deferred if pluggable modules stay good enough longer than anticipated. Two further risks: NVIDIA’s LinkX connectivity products could displace Marvell from the AI clusters it helped build; and accelerating decline in legacy segments (storage, enterprise — the remaining ~26% of revenue) could mask the true growth pace of the core datacenter business.

Bottom Line

Marvell holds a genuinely privileged position across several AI infrastructure bottlenecks, with monopoly or quasi-monopoly dynamics in optical DSPs and custom silicon. The investment case is real but concentrated — its fortunes are closely tied to a handful of hyperscaler relationships and the pace of AI capex. The central question for investors is whether current valuations reflect the captive, multi-year nature of these engagements, or treat them simply as market share gains in competitive end markets.

Stock Chart And Price Outlook

If equities melt, so too will $MRVL. But in a stable or up market, here’s how we view the stock’s potential. You can open a full page version of this chart, here.

The first step to a real bull run is whether the stock gets up and over $100 and holds over that level. If it does, $140 is possible.

A stop below the recent lows of $75 is a low-risk way to keep your position safe.

Alex King, CEO, Cestrian Capital Research, Inc, 8 March 2026

With support from Claude CoWork.