LUMN - Accumulate; PT $12 - Restructuring Almost Complete.

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Analysis by Alex King and “FredFrog” for Cestrian Capital Research, Inc; support from Claude CoWork.

Lumen Technologies ($LUMN) has spent the last three years remaking itself from a debt-laden legacy telco into what management intends to be an enterprise-focused fiber pureplay, serving the largest customers, a play on the AI boom. This transformation is largely complete; the company has a rapidly-growing, prepaid book of business as proof. We anticipate an uptick in revenue growth and cashflow margins, together with deleverage, as value drivers. The stock’s most recent close was $6.75; our price target is $12. A drop below $6 would invalidate our price target.

Update On Corporate Restructuring

Since 2023, under newly-appointed CEO Kate Johnson, Lumen has run one of the more aggressive corporate makeovers in US telecom, and it has come in four connected waves: pruning the portfolio, repairing the balance sheet, pivoting commercially to AI infrastructure, and finally exiting the consumer business altogether.

Portfolio pruning: In October 2023 Lumen exited the content delivery network business, handing customer contracts to Akamai (see our recent coverage of $AKAM earnings, here), and in November 2023 it completed the sale of its EMEA operations to Colt, a division of Fidelity, for $1.8 billion. These followed the October 2022 closing of the sale of 20-state incumbent local exchange carrier (ILEC) operations to Apollo-backed Brightspeed for roughly $7.5 billion.

Balance-sheet repair: Facing a wall of maturities, in late 2023 Lumen struck a Transaction Support Agreement with creditors that was expanded and finalized on January 25, 2024. The comprehensive recapitalization addressed more than $12.5 billion of debt — over 70% of Lumen and acquired Level 3 maturities coming due through 2027 — pushed those maturities out primarily to 2029 and beyond, and brought in about $1.3 billion of new debt plus a roughly $1 billion revolving facility. We can think of this as an amend-and-extend action rather than deleveraging.

Commercial pivot: Through 2024 Lumen launched its "Private Connectivity Fabric" service and signed more than $8.5 billion of new business selling custom, high-capacity fiber to the hyperscalers — Microsoft, Meta, AWS and Google — to carry AI workloads. This reframed Lumen's story from a shrinking telco to a picks-and-shovels supplier to the AI build-out.

Consumer divestiture: Announced in May 2025 and closed in February 2026, Lumen sold its "Mass Markets" fiber-to-the-home business — the Quantum Fiber operation spanning 11 states, more than one million fiber customers and over four million enabled locations — to AT&T for $5.75 billion in cash. Around $4.8 billion of the proceeds went straight to retiring superpriority debt, cutting long-term debt from about $17.4 billion at the end of 2025 to roughly $12.9 billion at the end of Q1 2026 and lowering annual interest expense by approximately $300 million. Alongside these moves the reporting structure was simplified: Lumen now effectively runs as a single operating segment focused on digital networking and strategic enterprise services, with revenue split between Business (Strategic versus Legacy) and Mass Markets (Fiber Broadband, Other Broadband, and Voice/Other).

Restructuring Not Yet Complete

There remains some long-tail business still to resolve at Lumen. Likely not through choice, the company retained its legacy copper-based Mass Markets operation — lower-speed residential and small-business broadband and voice running over aging copper in the old CenturyLink footprint. That business does not fit the enterprise digital-networking strategy and is in structural decline; it is the obvious remaining non-core piece, and we would expect it to be run off or sold over time. There are, needless to say, few buyers for such a business.

Leverage remains material at 4.7x TTM EBITDA but this is nothing unusual in telco; it is not inherently a risk. If cashflows improve as expected, management will have the choice of deleverage or other value creation methods (dividends, buybacks etc.).

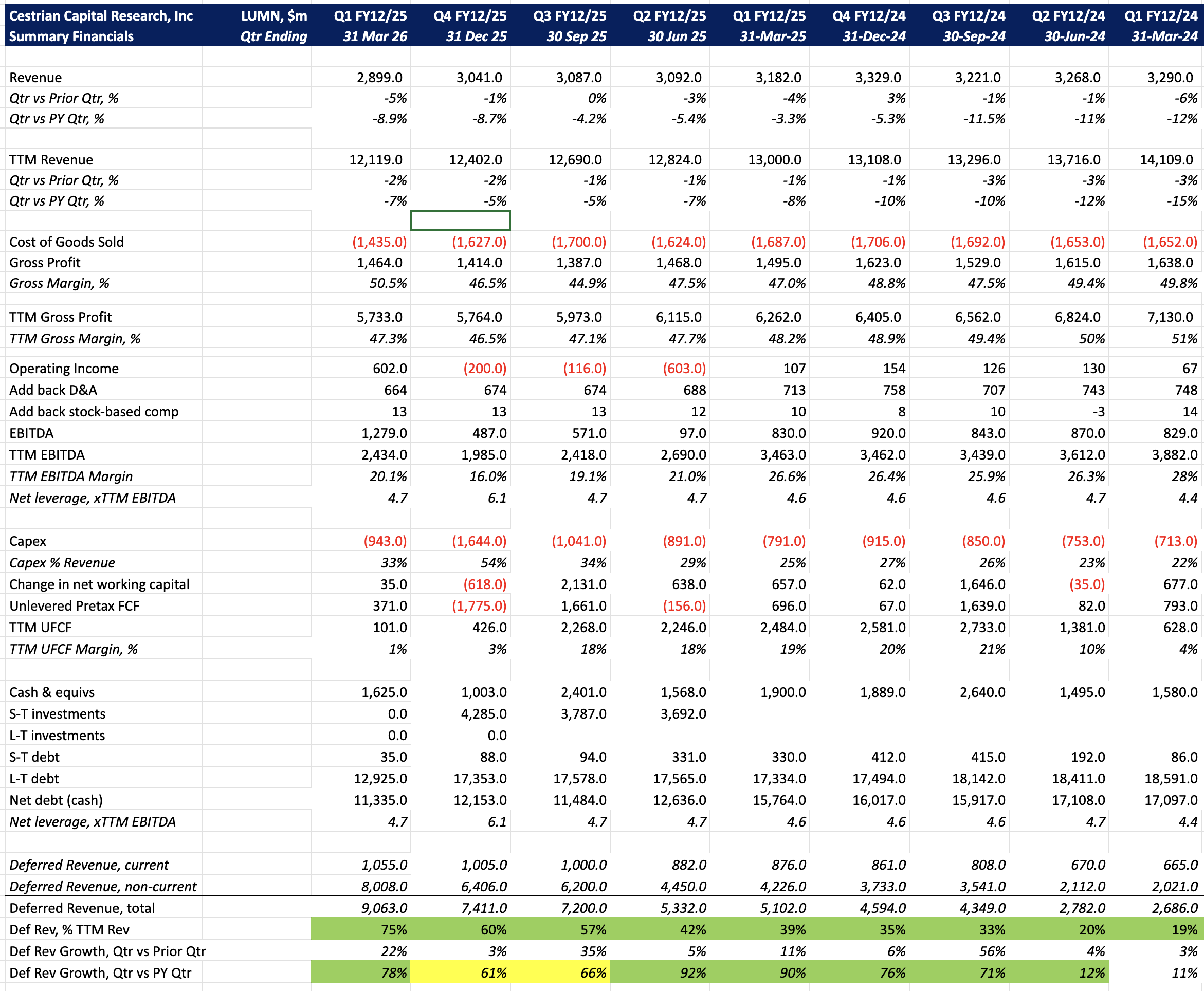

Q1 Earnings Review

Extensive restructuring means that time-series data alone doesn’t give us a particularly clear perspective on the company’s progress. Of main import today is the leverage multiple - perfectly acceptable - and the size and rate of growth of the deferred revenue book. Deferred revenue, as you will be aware, represents contracted, already-invoiced business which has yet to be delivered. As of the end of March 2026, total deferred revenue represented 75% of TTM recognized revenue - that’s high in telco - and was growing at a rate of 78% pa. Most likely that growth rate starts to tail off as the virtually-pure enterprise-focused business becomes the new normal; but deferred revenue as a % of TTM revenue should continue to grow as more non-core revenue is shed from the trailing number.

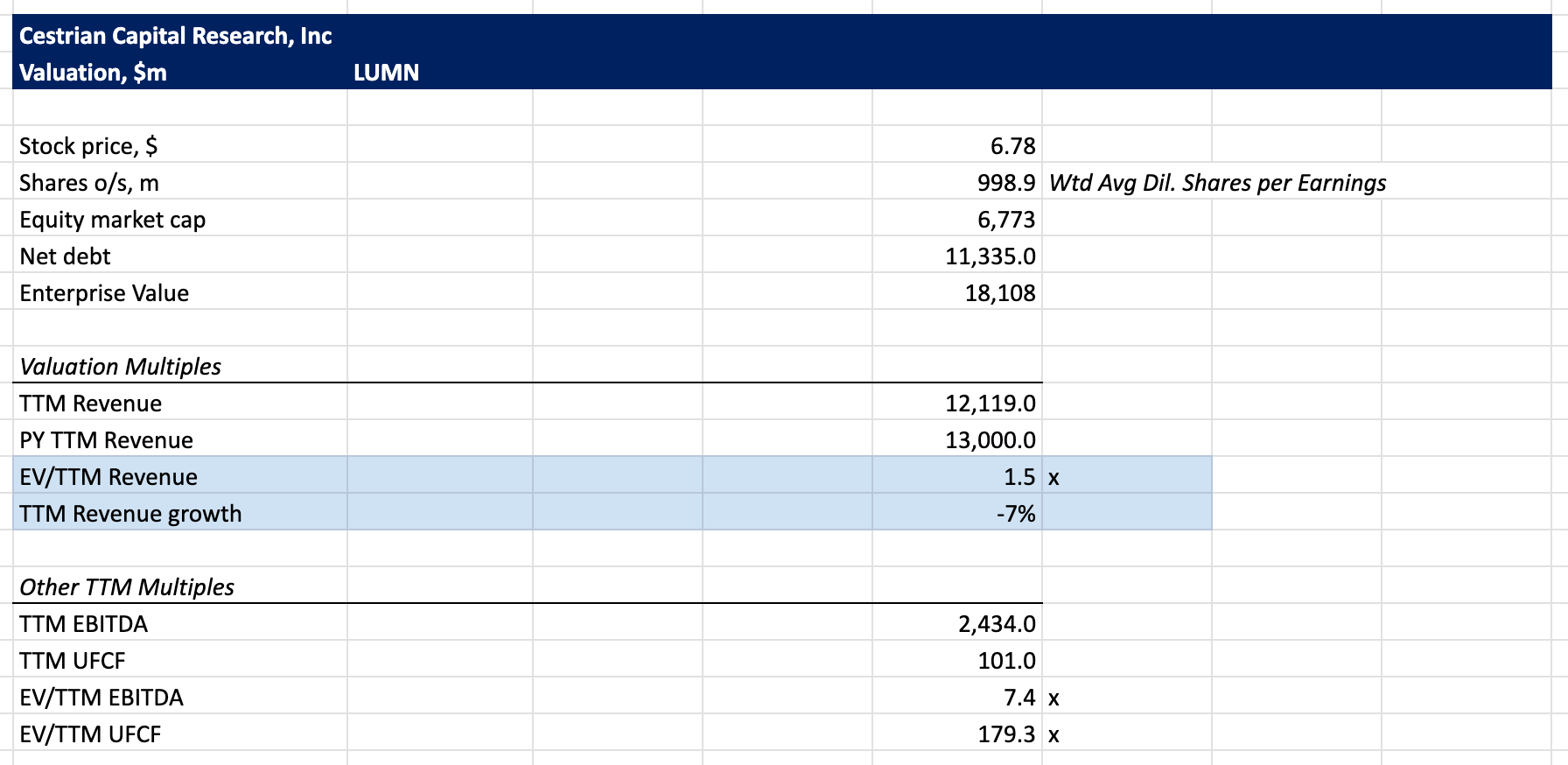

Valuation

Valuation metrics are more than usually useless at present. The company has provided no explicit revenue guide for FY12/26. We can safely ignore ‘adjusted EBITDA’ because it’s always best to ignore ‘adjusted EBITDA’ whenever you see it mentioned. And capex will likely overwhelm operating cashflow generation this year as the buildout of enterprise fiber remains intensive. All we really have to go on is an EV of 1.5x TTM revenue at present; revenue likely declines in FY12/26 as slowdown in copper revenues weigh on acceleration in fiber; so a forward EV/Revenue is probably in the 1.6-1.8x range, which is neither cheap nor expensive in my view.

Stock Chart

LUMN is volatile, as its corporate story would suggest. The stock looks to have found support in the $6.10-$6.30 range. Using a standard Elliot Wave pattern to project where the stock may go next, I think $12 is a reasonable target (it’s a little above recent highs and represents the 100% extension of the Wave 1 shown, placed at the Wave 2 low). $18 is a potential stretch target but I would not hang my hat on it. My expectation is for a cooling-off if the stock tops out in that $12-18 range. And if the stock fails to launch but instead drops below $6, then something bad is happening and I myself would sell and get out.

We rate the stock at Accumulate between $6-$8.25 based on the volume x price profile evidencing institutional buying in that range . You can open a full page version of this chart, here.

Questions, Further Analysis Required?

If you’re not yet an Inner Circle member, you can join here as an independent investor, or contact us at minerva@cestriancapital.com if you are an investment professional. As an Inner Circle member, you can reach Cestrian analysts round the clock in our Slack environment, get advance notification of all Cestrian staff personal account trades including stop details and capital allocation levels by position, and much, much more.

Cestrian Capital Research, Inc - 10 July 2026

DISCLOSURE: Cestrian Capital Research, Inc staff personal accounts hold long positions in $LUMN.