Microsoft Q3 FY6/26 Earnings Review (The Cestrian Circle Newsletter - NO PAYWALL)

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

by Alex King, CEO, Cestrian Capital Research, Inc.

Microsoft ( $MSFT ) is in a pickle. It made its early AI bet on OpenAI which initially looked very smart, but which has proven troublesome. It’s early in frontier-model land and whilst Anthropic looks to have the lead on everyone right now, that could be just down to a superior IPO marketing plan. No need to rule OAI out of contention yet; but we can say for certain that Altman is more of a handful than Nadella would likely prefer, and we can also say for certain that if Microsoft had the equivalent of CoWork then it would be doing many victory laps about its AI strategy. It is not, and the stock is playing witness to that.

But.

The numbers at MSFT are good and the stock chart looks bullish, at least for a reversal-of-sentiment play. People still think software is dead and the ups in software stocks continue to take these people by surprise, so for that reason alone there is probably some money still to be made in MSFT stock. Beyond that they are actually going to have to evidence their vision and blah for actually valuable AI applications.

Our Inner Circle members received a trade disclosure alert on this real-money purchase of MSFT on 19 May - right now that’s up +8%.

I remain long the stock.

Let’s take a look at the numbers, the valuation, and the stock chart.

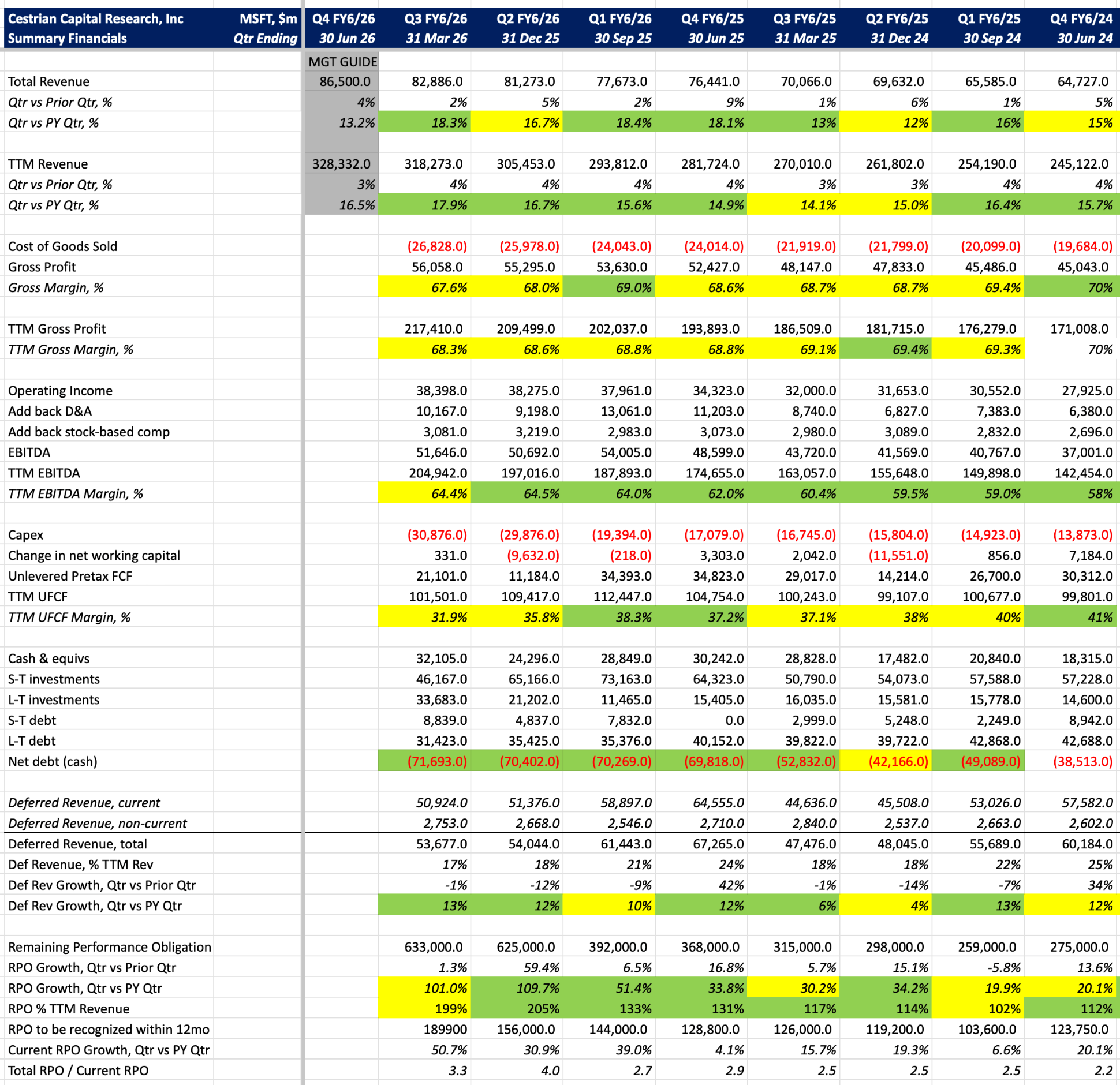

Microsoft Financial Fundamentals

Very strong numbers.

- Growth accelerated to +18.3% vs. the same quarter last year and +17.9% on a TTM basis vs. prior year; that said, the guide indicates a slowdown into next quarter.

- Gross margins are holding up fine; cashflow margins are in decline but remain very strong at 32% on a TTM basis - compares very favorably to other asset-light names which are also now capex monsters.

- The balance sheet has $72bn of net cash, enough to keep the wolf from the door.

- RPO - order book - growth slowed a touch but it remains growing at >100% vs. this time last year.

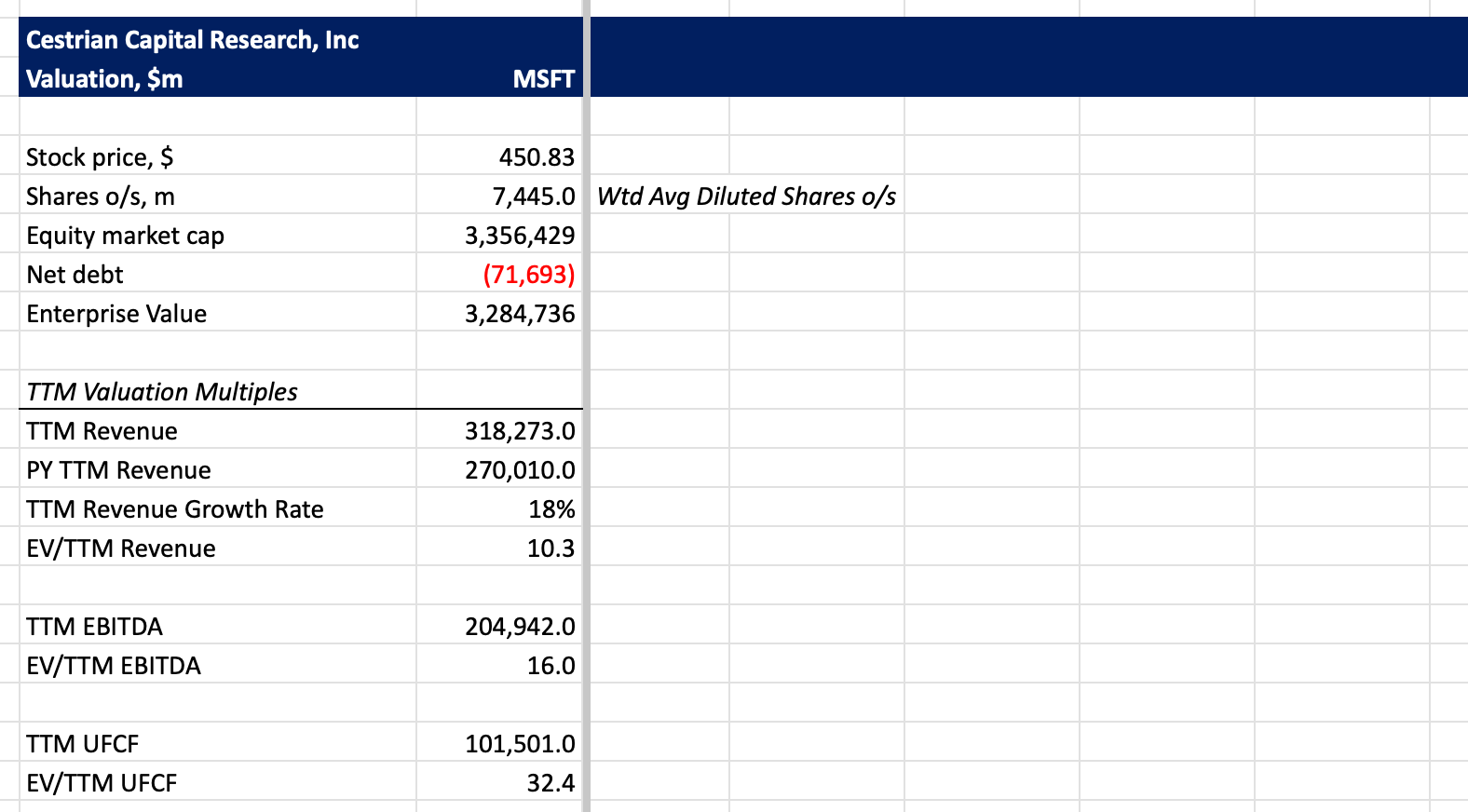

Microsoft Valuation Multiples

The valuation is betwixt and between. No particular reason to buy or to sell the stock on these multiples alone.

Microsoft Stock Chart And Rating

You can open a full page version of this chart, here.

The stock is up some +27% from its 2026 lows already. The 200-day SMA proved too much today and the stock sold off a little having rejected it. I suspect the stock will take another run at the 200-day before too long. I think weakness will be supported at around $425, the top of the high volume nodes below.

The easiest risk/reward trade to consider now is to wait to see if MSFT crosses up and over the 200-day and then, if you see a daily close above it, enter a long trade with a stop a little below the 200-day.

Personally I am long MSFT already, per the above disclosure alert shared with our Inner Circle members on 19th May. I am holding and, indeed, we rate the stock at Hold.

Cestrian Capital Research, Inc - 1 June 2026

DISCLOSURE - Cestrian staff personal accounts hold long position(s) in, inter alia, MSFT.