Moderna (MRNA) - Q4 2025 Review

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

The Fast Track Ends; The Lawsuits Continue

Nathan Brinkman

Moderna completed the fourth quarter with a balance sheet still fortified by pandemic-era cash generation, but continues with a business model still fully exposed to the volatility of a post-COVID commercial environment. Q4 results reflect a company in transition, from a pandemic-driven revenue engine to a late-stage development and launch organization attempting to build a multi-product mRNA franchise. COVID vaccine sales continue to normalize amid weaker booster uptake and seasonal variability, while operating discipline and pipeline execution are increasingly central to the equity story.

At the same time, regulatory uncertainty has become a meaningful overhang. Shifting global vaccination recommendations, evolving strain-selection timelines, potential changes in U.S. public health policy, and heightened scrutiny on updated vaccine approvals should introduce significant variability in new product registrations. Upcoming programs will require regulatory alignment on immuno-bridging endpoints, correlates of protection, and post-marketing commitments. These will materially influence launch timing and commercial ramp of the Moderna pipeline.

Even though Moderna received a refusal to file letter from the FDA for mRNA-1010 (seasonal flu vaccine), they are still guiding to a 10% revenue increase for FY2026, surprising the market. As I write this, MRNA is up almost 10% after the release of the Q4 financials.

What’s next for Moderna, let’s have a look.

Pipeline

In my opinion, the biggest concern for Moderna right now is pipeline delivery due to regulatory uncertainty. The FDA’s refusal to file letter has put a big question on delivery timelines and post marketing commitments. Specifically, approvals in the US for Flu (mRNA-1010), Flu + Covid combination (mRNA-1083), and norovirus (mRNA-1403). What’s uncertain is how the changing FDA will view the Oncology portfolio (mRNA-4157 in collaboration with Merck) and what challenges may result from the negative perceptions around mRNA technology. Even though those programs remain on track and show promising data, I think the current regulatory environment is important to consider on the future valuation of Moderna.

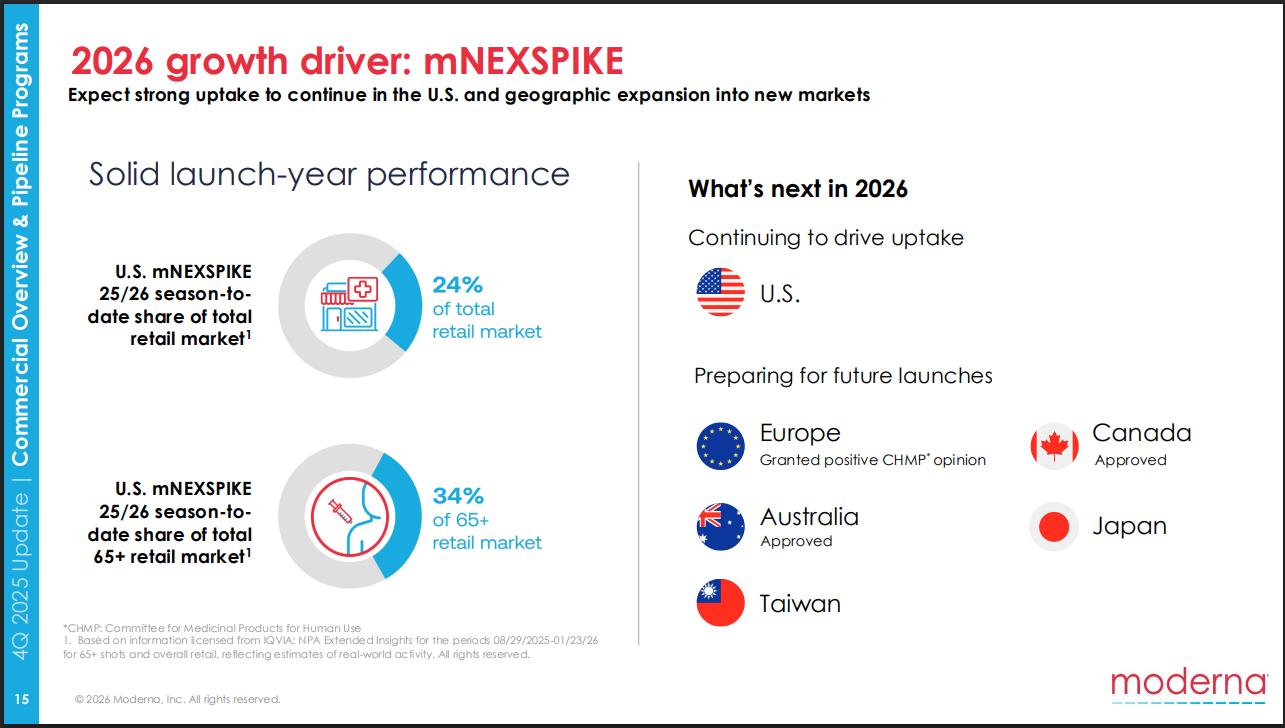

However, short term pipeline focus will be on geographical product expansion (outside of the US) as drivers of FY2026 revenue growth.

Moderna Q4 Presentation

Although I like the pipeline progress and indication focus, I don’t like the current regulatory environment right now, especially in the US.

Market Potential

No significant change to market potential from last update. However, concerns over mRNA perceptions and potential unwillingness for uptake in certain populations should be considered.

Partnerships / IP Position

In, Particles, Patents, Pandemics, and Plaintiffs, I highlight my concerns with Moderna’s IP position and will not repeat it in this summary. You can view the article here.

Funding / Cash Position

Moderna remains very cash heavy and is still able to fund its portfolio beyond 24 months. However, potential ongoing patent litigation with Aburtus Biopharma (ABUS) may change this in the near future.

Regulatory Position

Moderna retains its regulatory designations for some of its most important pipeline products, however, regulatory perception of the current infections vaccine pipeline is of concern. How this will spill into the company's pipeline for other indications is yet to be tested.

Current Regulatory Designations:

mRNA-4157 (personalized cancer vaccines)

- FDA Breakthrough Therapy Designation (granted February 2023; for melanoma in combination with Keytruda)

- EMA Priority Medicines (PRIME) Designation (granted 2023)

mRNA-1647 (Cytomegalovirus vaccine)

- FDA Fast Track Designation (granted 2019)

Financials

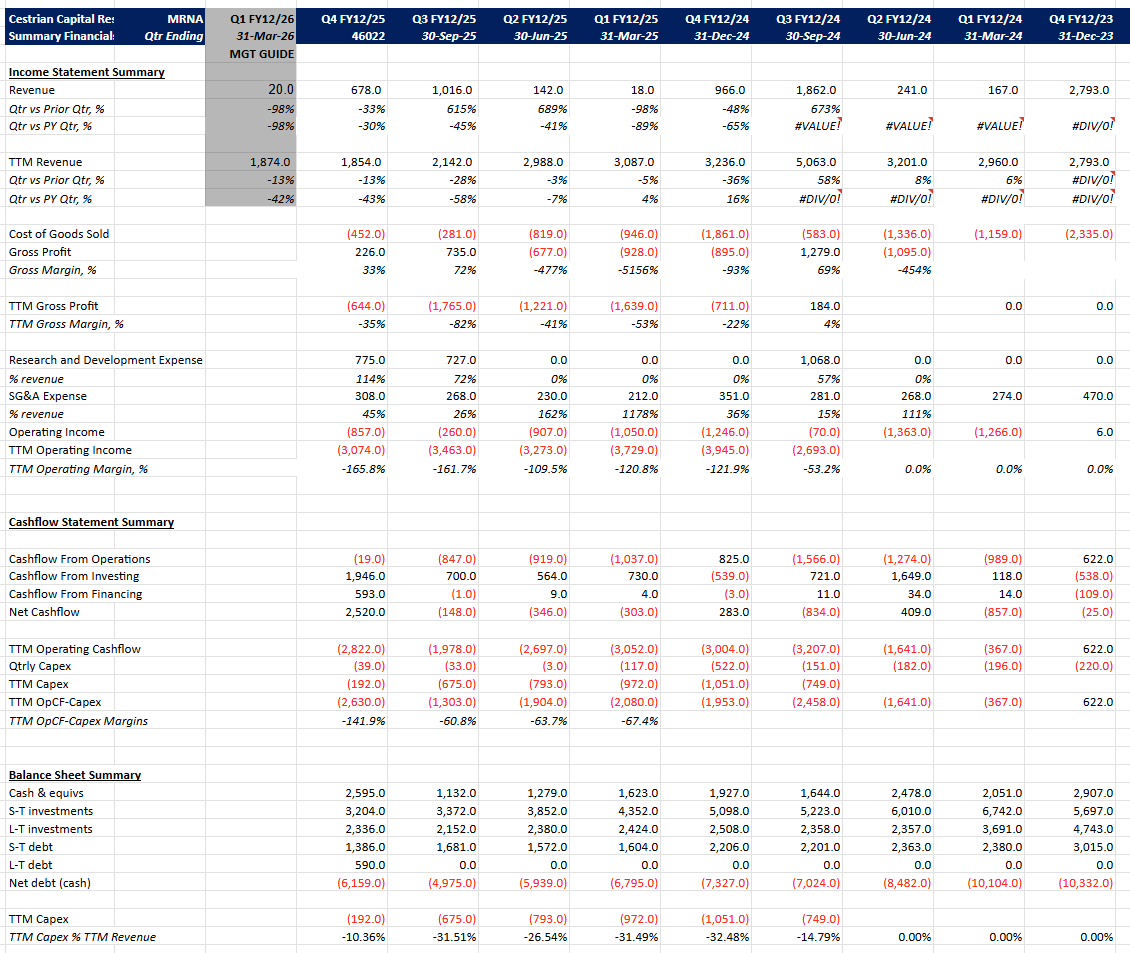

- Q4 2025 revenue at $678 mil. (-33% from previous quarter, -30% from PY quarter)

- FY 2025 revenue at $1.854 bil. (-43% PY revenue)

- Increasing cash on hand vs. last quarter, follows past post seasonal Northern Hemisphere COVID sales.

Valuation

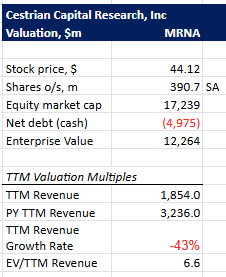

EV/TTM currently at 6.6 on 2/13/2026. Baseline is currently 5.95. Moderna seems to be trading at a valuation similar to its peers at the moment.

Chart

L-T (Weekly) - volume price profile at the ATH

Chart still showing what appears to be significant accumulation between $22-42 / share.

You can view the full page version here.

S-T (4-hr)

Zoomed in to the recent price action, one could make out a potential wave pattern here. Maybe it will get close to $62 in the short term, but I’m not sure.

You can view the full page version here.

Conclusion

Moderna’s near-term fundamentals are pressured by declining COVID revenues, lack of RSV vaccine uptake, high R&D investment and regulatory uncertainty. However, there is still pipeline potential which could drive long term growth in potentially high revenue indications.

Due to the current regulatory environment and questions around IP litigation impact, we rank MRNA as DO NOTHING.

I’ll revisit MRNA in Q1 2026 where we should have insight on both the regulatory requirements and IP litigation and may drop coverage in favor of other opportunities.

Author's Disclosure: Nathan Brinkman currently has no position in MRNA.

Cestrian Capital Research, Inc - 14 February 2026