Palo Alto (PANW) Q2 FY7/26 Earnings Review

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Bulking Up to Meet the Challenge

By Hermit Warrior a.k.a. Richard Iacuelli

As AI agents become autonomous employees, the old security playbook is not just slow, it's obsolete. Security must operate in real-time at the critical control points where decisions are made across network, endpoint, cloud, browser and identity. This is where Palo Alto Networks operates. And as AI becomes more embedded across the enterprise, those control points are converging.

A fragmented defense of disparate products is no longer a viable strategy. The risk is simply too high when adversaries are moving at machine speed.

Nikesh Arora CEO, Palo Alto Networks

House View

Whether by design or sheer dumb luck, the end result is what counts - and by that measure Palo Alto Networks (PANW) seems to have hit the nail on the head. From a strictly commercial strategy, to what is in today's age of autonomous agentic AI a potentially vital technical imperative, Palo Alto's pivot from discrete cybersecurity product vendor to a holistic platform provider ('platformization' in PANW-speak) is driving what promises to be a step-change in their market positioning and growth prospects.

This has not come without significant investments in expanding their capabilities, partly organically, but with most of the heavy lifting coming from a series of acquisitions, large and small. The net effect is the 'bulking-up' of Palo Alto Networks to rise to the challenge of expanding 'attack surfaces' and threats to infrastructure that come at machine speed.

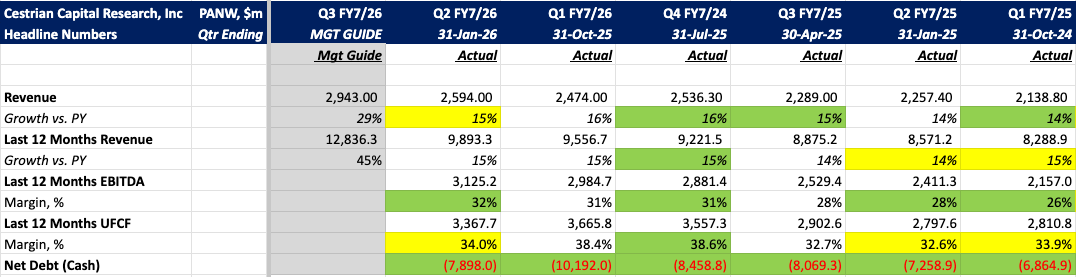

Here are the headlines.