This Is Our Top Pick In Tech

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

… and it was built on Sachertorte. Probably.

by Alex King, CEO, Cestrian Capital Research, Inc.

This note is for Inner Circle members only. If you’d like to join our Inner Circle service, you can do so from the links below; or reach out to me personally at alex.king@cestriancapital.com .

ARM Holdings ( $ARM ) was born in a low power environment. This storied company’s origins can be traced back to the classical tradition of technology startups, wherein a cash-starved team co-headed by a Mitteleuropean emigre needed to build low-power processors for a state-sponsored ‘universal computing’ project in the UK in the late 1970s and early 1980s.

The ensuing reduced-instruction-set (‘RISC’) architecture and by-design low power hardware requirements were the basis for a gradual evolution from hobbyists to a company whose IC designs now power most every smartphone on the planet. For many years ARM struggled to make inroads into the datacenter, because power requirements were not supreme until LLMs started to require so much matrix algebra and real-time storage that power grids became unable to keep up with the rate of rising power demand from the datacenter sector. But here we are.

In a world where Nvidia, AMD and Intel can sell you brute-force-compute, useful for training primarily, and in a world where ultimately inference (content creation) is where the value lies, ARM is without peer today. Its designs - licensed by ARM, and manufactured on their behalf by TSMC or Intel, not manufactured in house - licensed - live at the center of most all ASIC and other special purpose chips that are in use and under development to handle the explosion of inference demand.

The next trend in LLMs - small-scale models using less intensive algebra to solve discrete tasks - suits ARM perfectly. This is true of the datacenter and it is also true of the endpoint, where we will soon see more LLM calculations being performed. iPhones with the A19 processor onwards, and soon-to-be-released Macs, will have the processor, memory, and software capacity to handle a lot of this stuff on the client side. All of the above run on Apple silicon which runs on … $ARM.

The company is, I believe, poised to experience sustained growth in orders and revenue and with that cashflows, since the business model is inherently high margin. Better, the stock is in the doldrums, in great contrast to where $NVDA, $AVGO and other sector leaders sit today near their all time highs.

We are at a tricky time in this market, not a time to go all-in on anything really; so if ARM interests you and you don’t have a position, you might think about this simple method:

- Open a position, sized to suit your risk appetite

- Place a sell-stop-limit somewhere below $100 (that was today’s intraday low post earnings) - this way if the selling takes ahold of ARM you will be out with a modest loss.

- If the stock moves up, watch to see if it clears and closes over the 21-day EMA (currently at $111, not coincidentally that is precisely one nanometer above the closing price today). If it does, you could move your stop to a little under that 21-day EMA. If it clears the 50-day at $119 (currently) you could move your stop up to a little below that. And so on. Or just full-port-YOLO, I don’t know - you will do what’s best for you. I am saying that for me, some careful risk management is in order at present.

Price target? I think it can make new all-time-highs, which is to say $189 or better. Not tomorrow. But I think it’s possible.

You can open a full page version of this chart, here.

That looks to me like accumulation down here - the high vol x price bars define our Accumulation Zone. For risk levels and stops, see above.

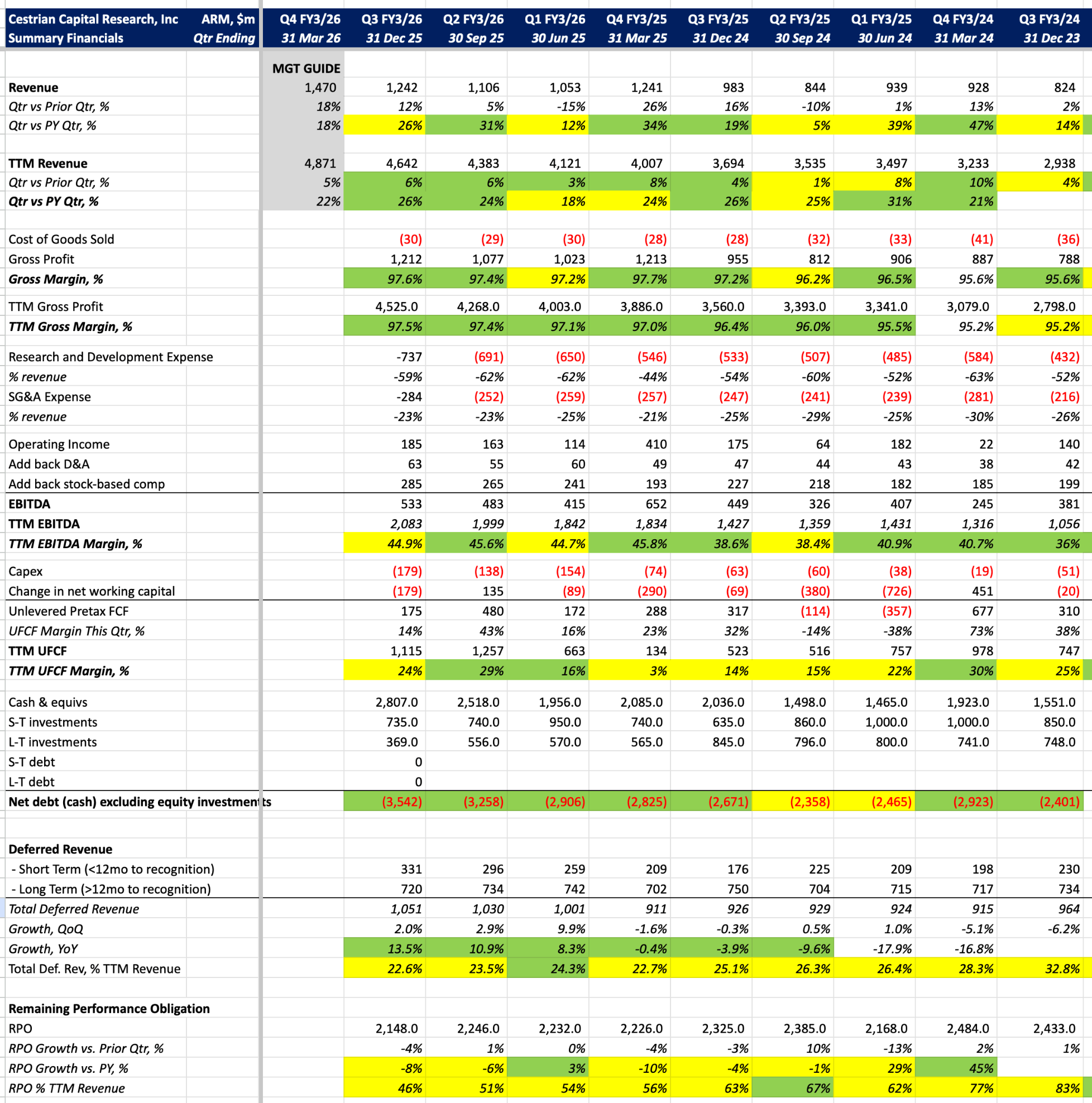

Numbers are in the “good” not “great” category, including RPO which to be honest I would think would be spooling up more than it is. But recall in 2022/23 NVDA stock started climbing quickly even when revenue was flat. Price runs ahead of fundamentals, always. (Not least because the fundamentals are weeks old by the time they are published, and because the conversation with customers that is yet to translate into orders has yet to make it into the RPO number).

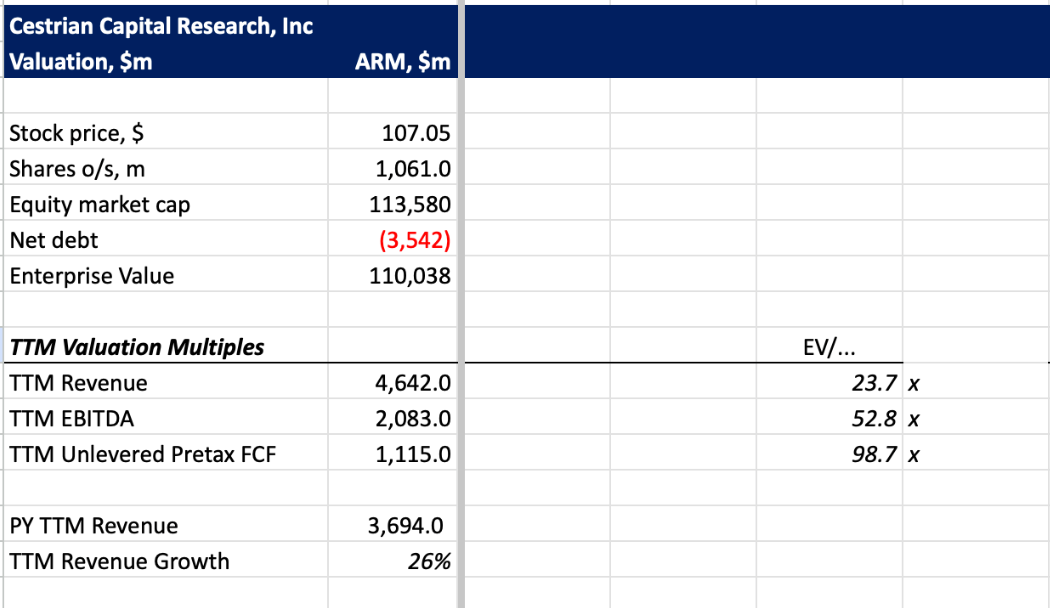

Valuation is punchy, no doubt. Makes NVDA look cheap.

But no-one ever said that the big potential winners would be easy. In short - I think this one can be bought up by the crowd if it continues to win share in inference, and I think that a logical stop can be placed fairly close to the current price. In short I believe risk/reward is set up pretty well.

Cestrian Capital Research, Inc - 5 Feb 2026

DISCLOSURE: Cestrian analyst personal accounts hold long positions in, inter alia, $ARM.