What If … All That Capex Was Good? ORCL Q3 FY5/26 Earnings Review - and More (NO PAYWALL)

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Oracle Q3 FY5/26 Earnings Review And More

by Alex King, CEO, Cestrian Capital Research, Inc with help from Claude.

Oracle ( $ORCL ) has had a bad name since it pulled the RPO rabbit out of the hat last year, with the razzmatazz of a big order from OpenAI seemingly blinding investors to the changing fundamentals of Oracle. No longer an asset-light software business using its cash to lever up and buy back stock - the effect being to boost founder Larry Ellison’s personal cash pile - Oracle is now in the business of building and filling datacenters. The debt required to do so has raised eyebrows and is associated in investors’ minds with the stock collapsing from $346 down to $134 in less than six months. With the earnings print just in, the stock is presently at $163 in post-market trading.

The fear surrounding the company’s datacenter financing is real, and not silly. The counterpoint is: in essence this whole thing is a bet on black, which is that continued datacenter spend is good and will generate a return someday. Everyone assumes this will be a bust, which is why the stock is down so much.

But will it? Or could the Oracle (Once) Of Redwood Shores regain its crown?

Claude Assesses Oracle’s Balance Sheet Risk

Oracle's capital expenditure surge — now exceeding 100% of quarterly revenue — raises important questions about how the company is financing its massive datacenter buildout. Oracle has historically used a mix of on-balance-sheet debt and off-balance-sheet arrangements (including sale-leaseback transactions, build-to-suit leases, and joint ventures with infrastructure partners) to fund its cloud expansion. The operating lease obligations disclosed in Oracle's filings have grown substantially, and the company has also entered into significant financing commitments that don't appear as traditional debt on the balance sheet. This means the headline debt-to-equity or net debt figures may understate Oracle's true financial leverage and fixed obligations.

The core risk is duration mismatch and commitment rigidity. Oracle is locking in long-term lease and financing obligations (often 10-20 years for datacenter facilities) against customer contracts that, while large in aggregate RPO terms, may have shorter effective durations or contain flexibility provisions that allow customers to scale usage up or down. If AI infrastructure demand were to slow or shift to a competing platform, Oracle could find itself servicing fixed facility costs against a shrinking or slower-growing revenue base. The off-balance-sheet nature of some of these commitments makes it harder for investors to fully assess the magnitude of this tail risk from the face of the financial statements alone — one needs to dig into the lease footnotes and commitment disclosures in the 10-K/10-Q to piece together the full picture.

That said, there are meaningful mitigants. Oracle's RPO of $553B provides substantial contractual revenue visibility, and many of the largest cloud infrastructure deals reportedly include take-or-pay provisions that obligate customers to minimum spending levels. Oracle's operating cash flow generation remains strong, and the company's credit rating gives it favorable access to capital markets if needed. The risk is real but probably manageable as long as the AI infrastructure demand cycle plays out roughly as expected — the scenario where this becomes a genuine balance sheet problem would require a significant and sustained pullback in enterprise AI spending, which would be a sector-wide event affecting many companies beyond Oracle.

“Capex Is Bad” Bros May Be Wrong

All you ever read these days is lines akin to “when the big hyperscalers back off the capex, their stocks will moon!”. This is rather a negative outlook. It assumes all these top-tier companies are as effective in capital allocation as is Mr. Zuckerberg of META Platforms, who already canned his Metaverse concept in 2022 and may yet have to cut once more in AI. I think though that La Zuck may be an outlier and not the norm.

Let’s look at whether the ramp in capex at Oracle is capable of delivering the higher growth rate it is designed to achieve.

Capex is rising, both in the absolute and as a % of revenue; meanwhile revenue growth continues to accelerate. It might be a coincidence, it might be that this is a short term effect and the capex won’t continue to fuel an increased rate of growth in the future … but so far the facts are the facts. Capex up, growth up. Now, is it possible that the markets can learn to re-rate the multiple of stocks that work this way? I think it is. Markets understand “raise capital, deploy capital, create value from the capital deployed” very well, and once a big shop like ORCL can evidence that this method is working, I think they will be looked up on most kindly.

At some point, the cashflow generated by the company has to more than pay for the capex; I think that will come as LLM efficiency grows. We are already seeing Anthropic report lower hardware intensity requirements - the other LLM providers will follow suit I think.

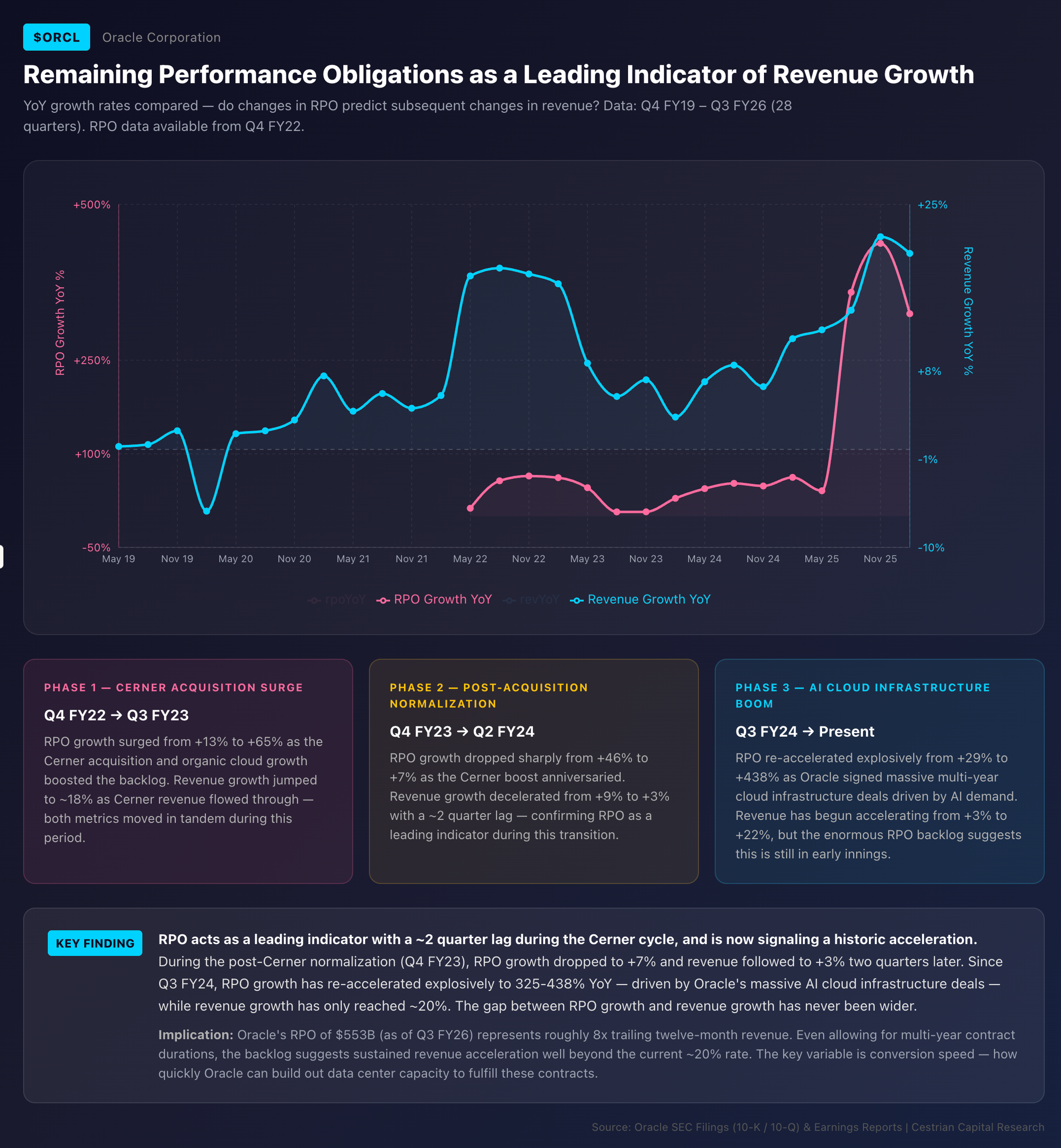

RPO Leads The Way

Another reason to be cheerful is that the growing Remaining Performance Obligation (RPO) is leading the increasing rate of revenue growth too. So you have two factors at play; capex >> infrastructure upon which projects can be run >> orders for those projects which show up in RPO >> revenue growth rate up. This is good.

After Claude pulled all the historic numbers from the SEC, I asked it to assess whether RPO growth increases have lead to increased rates of revenue growth at ORCL. The answer is a “yes so far”.

So with all this in mind let’s take a look at the company’s financials, valuation, and stock chart.

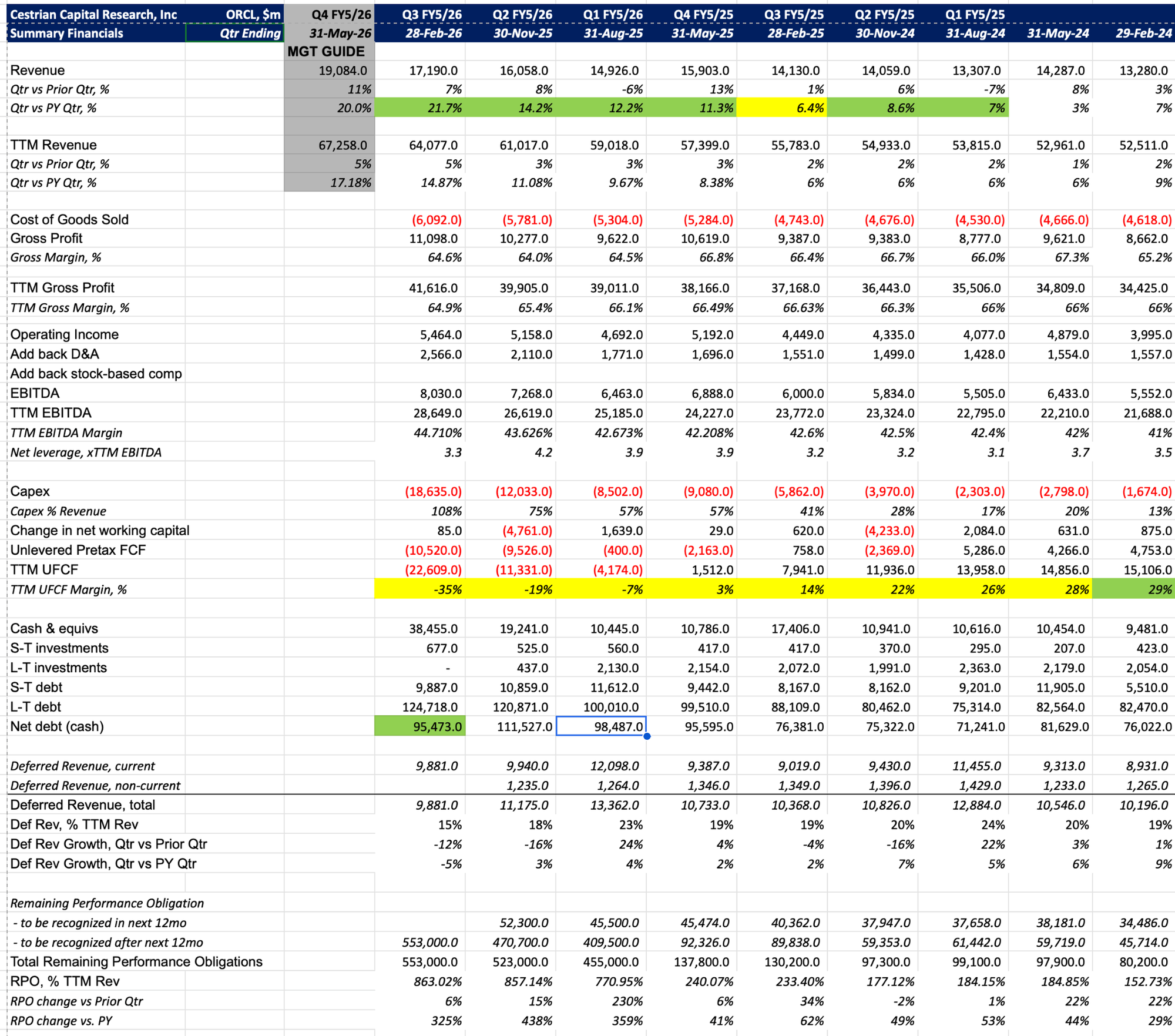

Financial Fundamentals

The lines to watch here are:

- Rate of revenue growth - accelerating, good

- TTM unlevered pretax FCF margins - falling, bad, you want to see this start to bottom out and move back up - the capex has to fall for this to happen.

- Net leverage - now down to 3.3x TTM EBITDA by the way which is not scary at all.

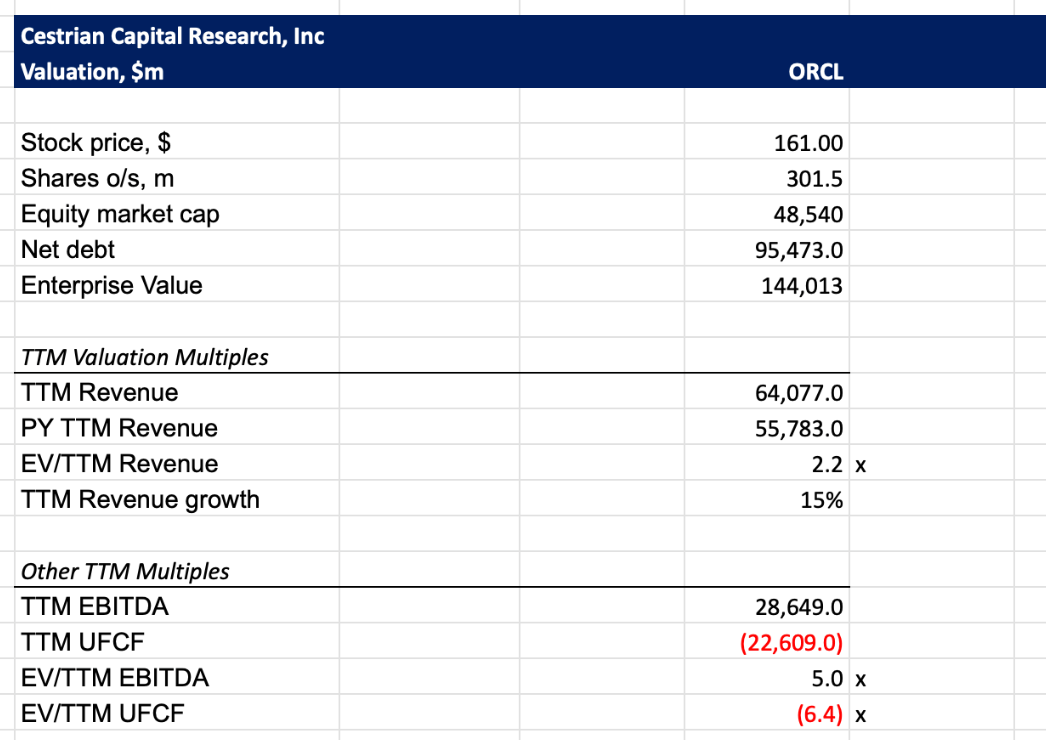

Valuation Multiples

The valuation is low. 2.2x TTM Revenue / 5x TTM EBITDA.

Stock Chart

Price is near a tradable low for stop-losses; and there is a lot of overhead potential from here. You can open a full page version, here.

Rating

We rate ORCL at Accumulate, subject to stop placed below recent lows.

DISCLOSURE: I am long $ORCL

Cestrian Capital Research, Inc - 10 March 2026