Zscaler (ZS) Q2 FY7/26 Earnings Review

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Deflated.

By Hermit Warrior, a.k.a Richard Iacuelli

…it won’t be long before billions of AI agents interacting with each other will have access to mission-critical applications and sensitive data. Just like users, an organization's AI agents are also becoming the weakest link in cybersecurity. Imagine a threat actor hijacking even one of an organization's AI agents, resulting in a serious breach. AI agents shift the threat landscape and operate autonomously at speeds far exceeding humans, exponentially increasing agentic traffic while compressing the time to prevent, detect, and respond to threats.

Jay Chaudhry, Co-Founder, Chairman & CEO, Zscaler

House View

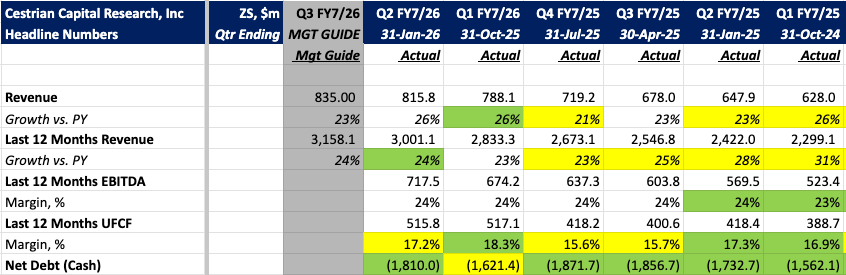

There was every reason to celebrate Zscaler's (ZS) Q2 results, released on February 27th, which were genuinely good, although shareholders must have wondered what happened to the party when the stock sank - yet again - post-earnings.

Revenues grew 26% year on year, well ahead of the 23% guide (and matching revenue growth in Q1), Annual Recurring Revenue (ARR), an important measure for many cybersecurity names, grew 25% to $3.4B - with management raising the full-year ARR guide to 24% - and the order book (RPO) grew 31% to $6.1B. On the profitability front, margins remained stable and non-GAAP operating income hit a record $181M. By most measures, this should have been a comfortable beat-and-raise quarter. It wasn't to be.

Perhaps it was the Q3 guide for 23% revenue growth (again), implying a deceleration in revenue growth, or maybe that the new 24% ARR growth target for FY2026 was only a touch ahead of the previous 23% guide. More likely, investors fret that 7% organic ARR growth, from an even more anaemic 1% in Q1, points to sluggishness in winning new business (RPO growth also decelerated from 34% in Q1). Added to persistently high Stock Based Compensation (SBS) at 26.5% of revenues, and continuing GAAP losses - larger in absolute terms than in Q1 - and the picture is perhaps not as bright as management were painting.

Regardless, Q2 results left the stock a little... deflated.

Here are the headlines.

Analyst Insights -

Growth:

Note: Management switched the regular earnings presentation format for a 'Shareholder Letter' so the 'slides' will fit a little awkwardly into this earnings review.

- Q2 revenue of $816M grew 26% year on year, comfortably ahead of the 23% guide and matching Q1's 26% — but only matching, not accelerating. Compare this to Cloudflare (NET), which delivered its third consecutive quarter of revenue acceleration in Q4 FY25, or CrowdStrike (CRWD), which has also posted two consecutive quarters of acceleration.