Zscaler (ZS) Q3 FY7/26 Earnings Review

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Falling Flat

By Hermit Warrior a.k.a. Richard Iacuelli

Sitting here today, our view is for total ARR and revenue growth for fiscal '27 of 16% to 17%.

Kevin Rubin, CFO, Zscaler

House View

A solid third quarter, at the headline level at least, elicited a brutal reaction - with good reason - as investors were spooked by not just one, but numerous negative signals coming from a management team that struggled to project confidence in the face of glaring contradictions. The market made its displeasure clear, with the stock falling as much as 32% the following day.

The catalyst for this dramatic reaction was not Q3 results, but FY27 guidance. Management took the unusual step of providing a preliminary FY27 outlook, forecasting ARR and revenue growth of just 16–17%, a sharp step down from the current 25% pace - and flying in the face of claims of AI providing the "strongest tailwinds our business has ever seen".

The cause, by management's own account, was three-fold: the abrupt departure of two sales leaders; 'tempered' assumptions on winning new large logo customers; and a lack of management conviction on the uptake rate for the new integrated SecOps offering (the Red Canary business) - all large red flags for reasons we'll explain later.

Layer on revenue growth already decelerating from Q2, and a CapEx driven guidance cut to free cash flow margins for FY26 of 22.8%–23.3% from 26.5%–27%, and an otherwise solid quarter was comprehensively overshadowed.

The competitive backdrop makes this awkward. As we noted in our Q1 and Q2 ZS earnings reviews, the central question hanging over Zscaler is whether its Zero Trust architecture can keep pace with PANW's platformization juggernaut. A 16–17% FY27 growth outlook — against PANW guiding to FY26 NGS ARR growth of 59%-60% (inc. acquisitions), CRWD's net new ARR growing 47%, and even FTNT accelerating to 20% revenue growth in Q1 — sharpens that question considerably. ZS is now, on its own guidance, potentially set to be the slowest-growing name in our cybersecurity coverage universe next year.

The Zero Trust technical architecture advantage is real and compelling. The mystery is why Zscaler have as yet been unable to translate technological leadership into sustained success in the market.

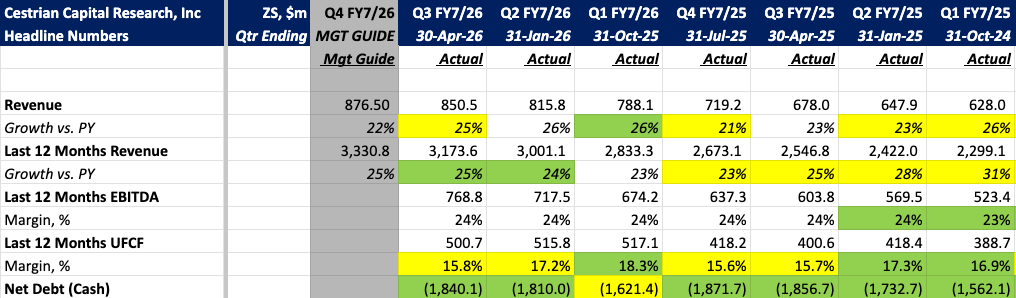

Here are the headlines.

Analyst Insights

Growth

- Q3 revenue of $850.5M grew 25% year on year, beating the 23% guide. Revenue growth has now held at 25–26% for three straight quarters, but is no longer accelerating as it briefly did in Q1. Compare to FTNT (20% and accelerating), CRWD (25.6% and accelerating), NET (34%), and PANW (31% headline, but high-20% organic NGS ARR).