BREAKING! Valley Dinosaur In Lazarus Shocker (NO PAYWALL)

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Michael Burry Is Right (*)

Alex King, CEO, Cestrian Capital Research, + Claude CoWork

(*) will delete if wrong

Everyone knows that Adobe is doomed. Your own good sense tells you this - image generation and control, and document handling, in the age of Nano Banana and Claude? Cmon. The stock chart tells you this.

Heck the CEO just told you this.

So you can stop reading now. Right? I mean that Big Short guy who is now just another Substack’r, just because he likes the stock, who is he to say?

The company printed earnings yesterday after the close, and they were good. You wouldn’t know it, because the stock fell on news of the CEO stepping down. Which is a bizarre price reaction really. If you look at the stock price performance you would say, well, the CEO has not delivered at all for shareholders of late. So you might reasonably think that his leaving would be a good idea for shareholders. In fact, if you thought that Mr. Burry and some of his buddies had been building stakes in the company - you might think that maybe, just maybe, that fact was connected with the CEO’s departure.

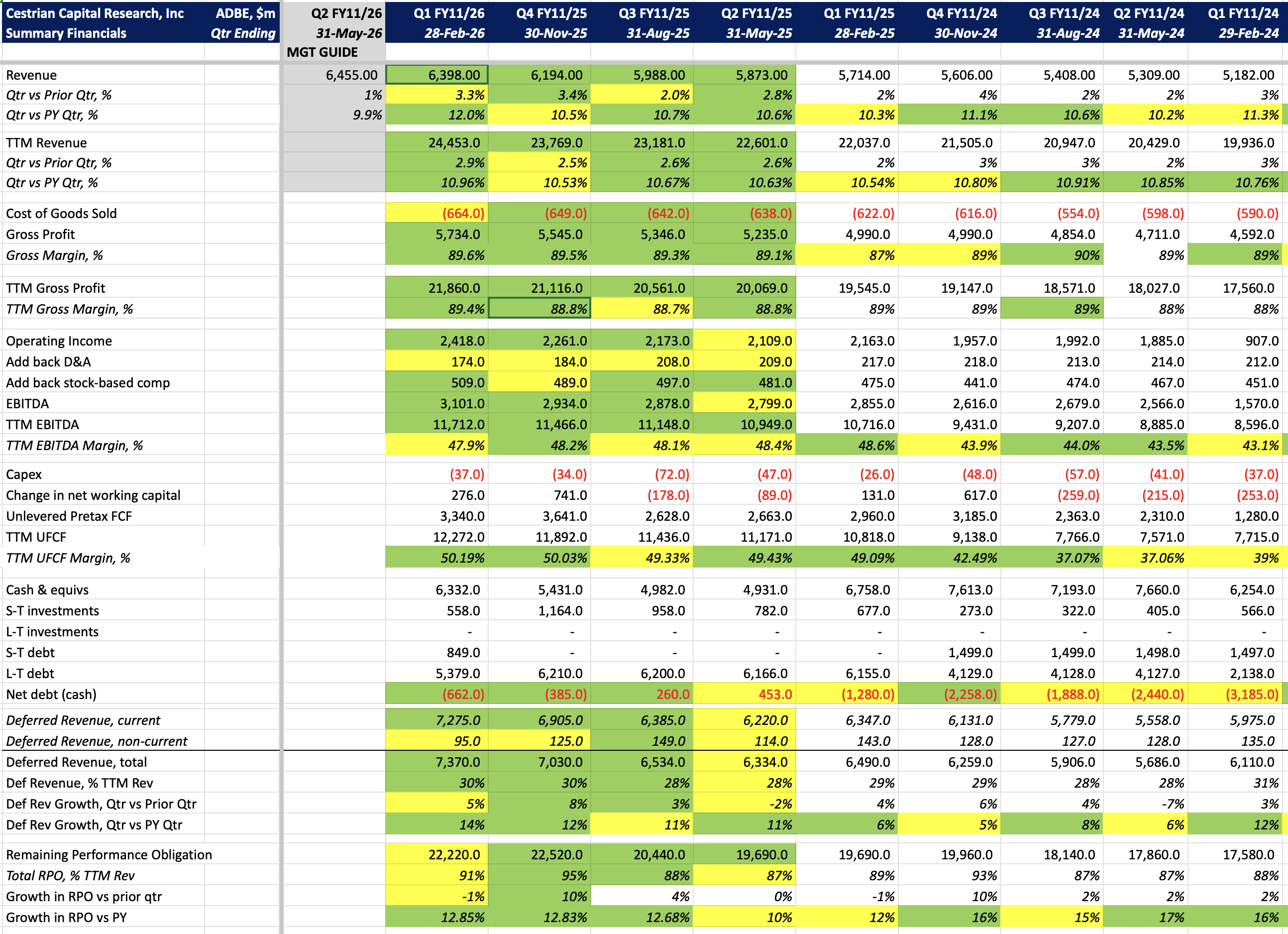

You see, the numbers were compelling. Let’s take a look.

Financial Fundamentals

- Revenue growth accelerated to 12% vs PY in the quarter, and to 11.0% vs PY on a TTM basis.

- Cashflow margins ticked up to 50.2% on a TTM UFCF basis.

- The company’s net cash balance rose a little to $662m.

It’s possible we see some further acceleration in revenue growth. Adobe’s order book (RPO) and deferred revenue (the prepaid element of the order book) both saw slight accelerations in growth rates. Looking at the historical relationship between deferred revenue, RPO, and revenue growth, the story is unclear when we look at deferred revenue; but RPO is a reasonable predictor.

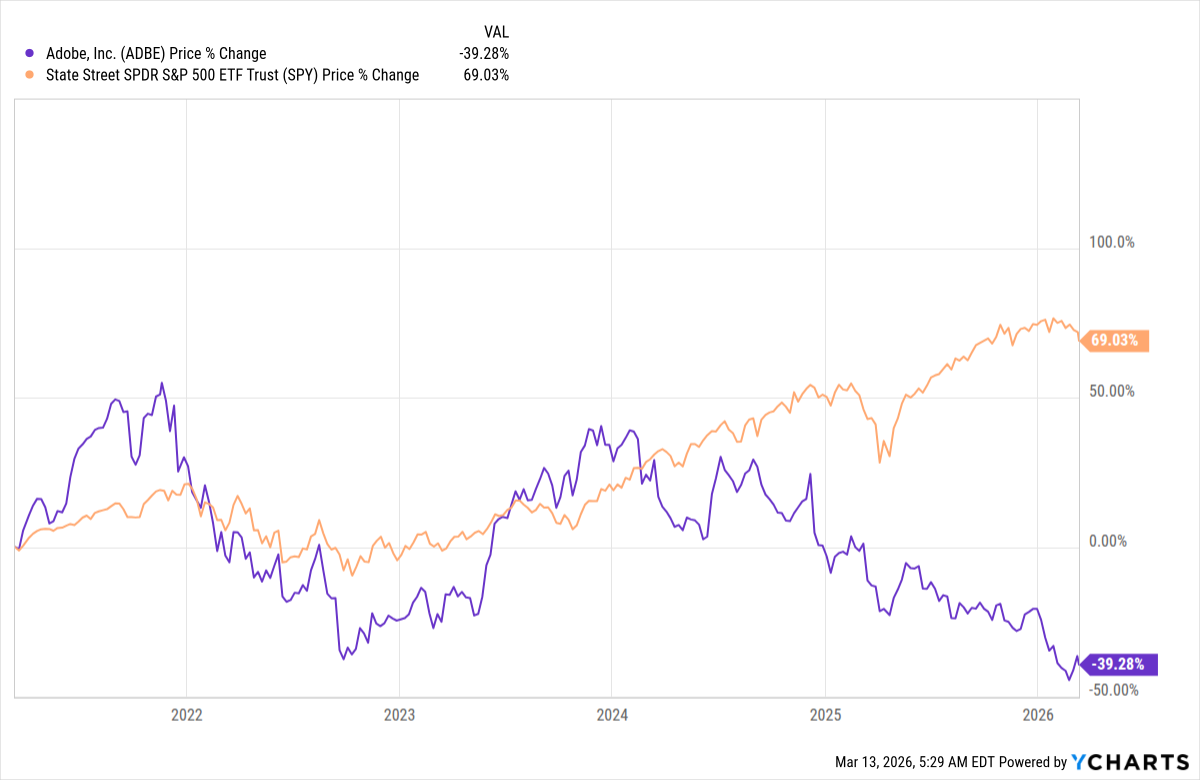

Stock Chart

The stock looks to me like it is attempting to put in a low. The selloff after hours and in pre-market trading today hasn’t made a new low. You can open a full page version of this chart, here.

The stock’s decline has been remarkable; it has shed more than 60% of all the value created since the GFC lows of 2009 to the ATHs of 2021.

So is it time to buy?

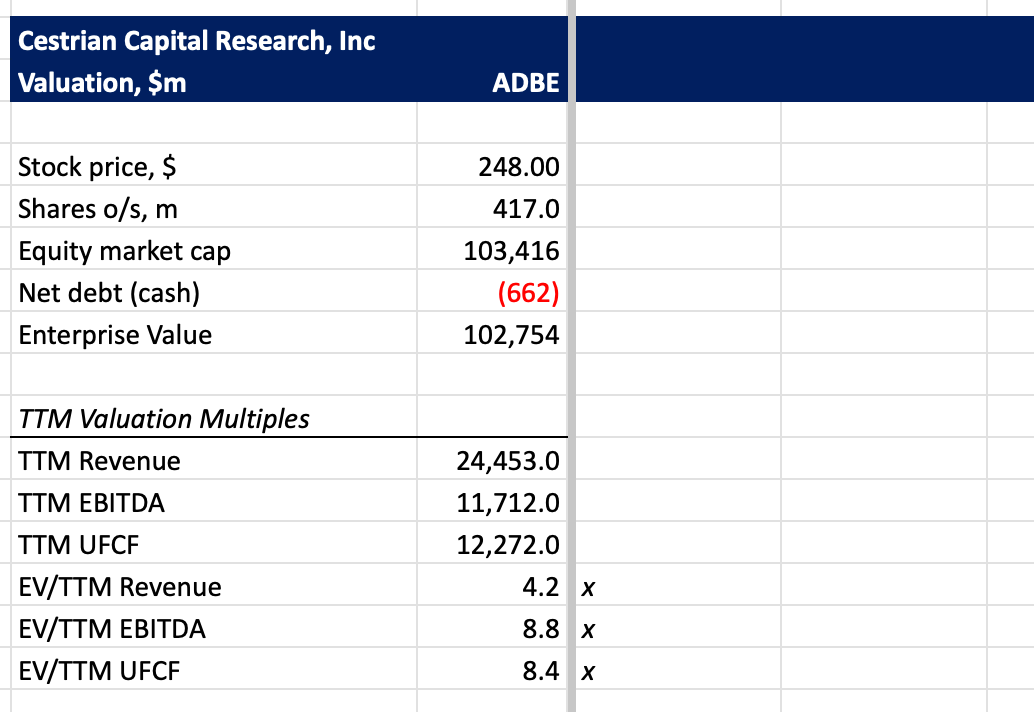

Valuation Analysis

Well, valuation at present is low in my view. 8.4x trailing cashflow for 11% revenue growth at 50% margins? That’s not at all expensive. That’s a multiple from 10-15 years ago in fact.

The Bull Case

The bull case for ADBE in the age of AI, by the way, is very viable in my view. Four key points are worth highlighting.

- Adobe owns the workflow, not just the tool. The bear case assumes AI image generation replaces Adobe — but most creative professionals don't just generate images, they compose, edit, retouch, mask, layer, and export them. Photoshop, Illustrator, Premiere and After Effects are where generated images go to be finished.

- As per other major enterprise software names today, Adobe is building AI into the product. Firefly — Adobe's generative AI model — is embedded directly into Creative Cloud apps. I expect to see this “AI Inside” method be touted all around Wall St by the big enterprise software companies in the next 12 months.

- Firefly's IP-clean training data is a genuine commercial differentiator. Enterprise and agency customers face real legal exposure using Midjourney or DALL-E or other such outputs commercially. Adobe trained Firefly only on licensed and public-domain content, and indemnifies commercial users. For any company with a legal department, this matters enormously and narrows the competitive field considerably. IN GENERAL - a big reason I expect corporate buyers to stick with existing enterprise software vendors is risk management. This is a good example of that.

- Pricing power is tilting upward. Claude believes that Adobe has been threading through price increases and tiered AI credit models. Firefly credits are now a monetization layer on top of subscriptions — effectively allowing Adobe to charge more for heavier AI usage - if true that will be an embedded source of revenue growth because AI usage is only going in one direction if you ask me.

The Bear Case

We all know the bear case, namely, this thing is getting commoditized, and that has lain behind the stock price performance these last few years. I think the bear case has actually happened, and now it’s time to re-assess.

Rating

We rate ADBE at Accumulate but for me that needs to be on a very tight leash. If the stock makes new lows, all bets are off; you want to see this name holding over the recent lows and you are looking for a move up on a new CEO announcement. In general, software looks bullish right now; I think it will lead the market up whenever the war in Iran de-escalates, allowing oil prices to fall back and therefore inflation concerns, bond yields and input costs to fall back too.

So for me I would consider opening a long position here but with a pretty tight stop below the recent lows. You, as always, will do you.

Cestrian Capital Research, Inc - 13 March 2026