CrowdStrike (CRWD) Q1 FY1/27 Earnings Review

Last updated on Jun 26, 2026

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

The Mythos Moment

By Hermit Warrior a.k.a. Richard Iacuelli

CrowdStrike is now being understood as critical AI infrastructure. Frontier AI Labs started a new chapter in the AI revolution. New model releases starting in April connected AI innovation with cybersecurity necessity.

George Kurtz, Founder & CEO, CrowdStrike

House View

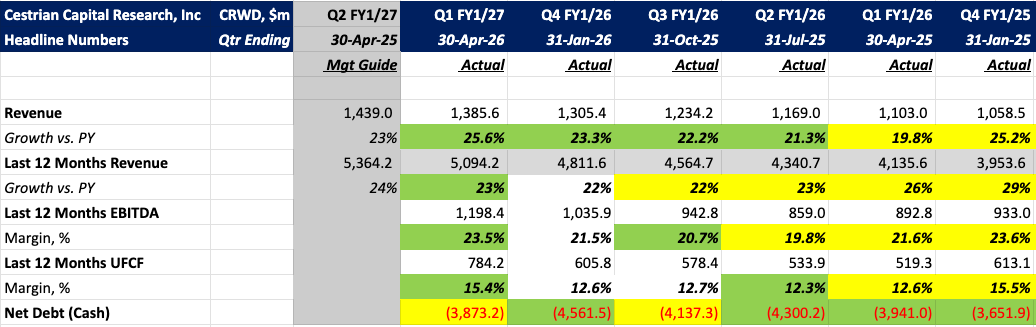

Record quarter, 10% sell-off — a pattern that by now feels oddly familiar across our cybersecurity coverage universe. CrowdStrike (CRWD) beat every guided metric, raised full-year net new ARR guidance by over $50M, posted all-time records in (non-GAAP) free cash flow, operating income and cash from operations, and announced a 4-for-1 stock split. The stock fell ~10% anyway. With CRWD up roughly 60% on the year going into the print and trading at nosebleed multiples, the bar was set in the clouds — and gave investors their excuse to take profits.

The quarter's defining feature centered on management's 'Mythos moment' commentary. CrowdStrike's argument is that the April release of 'frontier' models (Anthropic's Mythos, OpenAI's Daybreak) flipped a switch — cybersecurity went from being viewed as a cost of doing AI to being, in Kurtz's words, foundational AI infrastructure. CRWD was the only cybersecurity vendor initially selected into both Anthropic's Project Glasswing and OpenAI's Trusted Access for Cyber (TAC), and it parlayed that into Project QuiltWorks, an industry coalition bringing together the big GSIs (Global Systems Integrators) and - notably - insurers underwriting frontier-model risk.

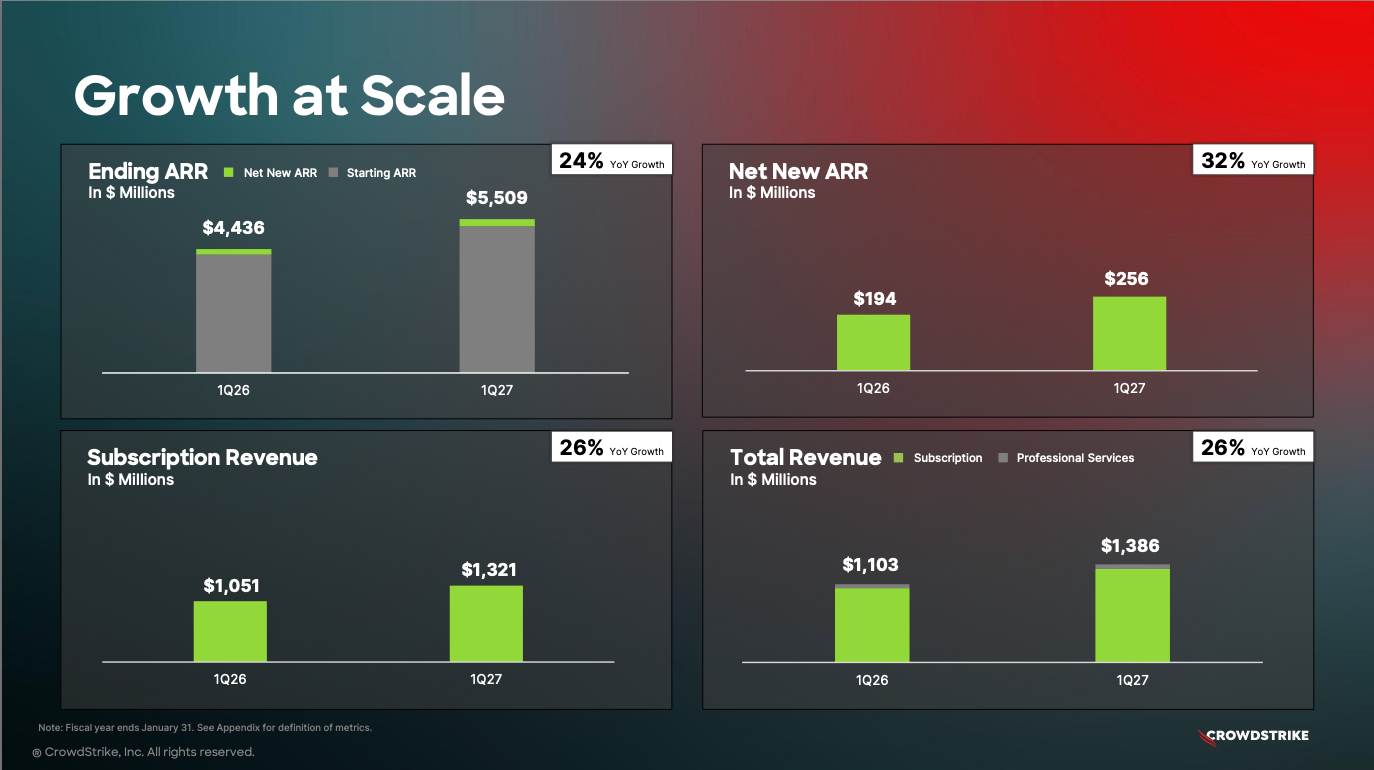

Whether the 'Mythos moment' proves a genuine inflection or a well-marketed quarter, the financials underneath it are notable: net new ARR up 32%, revenue growth accelerating for a fourth consecutive quarter, and AIDR — CRWD's AI-threat detection and response product — going from zero to a $50M+ pipeline in two quarters.

The peer read-across is striking. As we noted in our Q3 PANW review, Nikesh Arora made the same 'AI is a tailwind, not a threat' argument — and CRWD is now the second large-cap delivering hard numbers to back this up. The contrast with ZS (guiding FY27 to 16-17% amid sales-leadership turnover) and NET (restructuring 20% of its workforce - albeit for different reasons) could hardly be sharper. CRWD, like PANW, is accelerating into the AI wave rather than managing through a wobble.

The catch, as ever, is the price you pay for it. CRWD trades at one of the richest multiples in software, GAAP profitability is wafer-thin (a $27.8M GAAP net profit on $1.39B revenue), SBC remains heavy at ~21% of revenue, and a newly-launched Google Cloud AI Threat Defense platform is a reminder the hyperscalers are not standing still. None of this is new, and none of it is dragging on the business — but at this valuation, even a record quarter has to be perfect. Here are the headlines.

Analyst Insights

Growth

- Q1 revenue of $1.39B grew 26% year on year, handily beating the 23% guide and marking the fourth consecutive quarter of accelerating revenue growth (from 22% in Q2 FY26 through to 26% now). Compare to ZS (25%), PANW (31% headline but 14% organic), FTNT (20% and accelerating), and NET (~34%, slightly decelerating) — CRWD's acceleration through 26% at $5.5B scale stands out.