Palo Alto Networks (PANW) Q3 FY7/26 Earnings Review

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Steady as She Goes

By Hermit Warrior a.k.a. Richard Iacuelli

An AI model is only as effective as the data it can see. As [AI] frontier models become available to everyone, the real competitive advantage shifts from the model to the data fuel. That is why having sensors that sit in line with live traffic is so vital. They provide the telemetry and context needed to outmaneuver bad actors while serving as a critical enforcement point.

Nikesh Arora, Chairman & CEO, Palo Alto Networks

House View

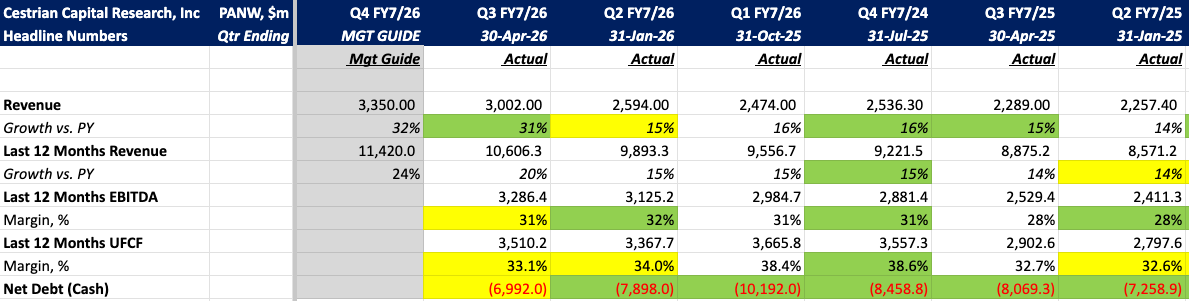

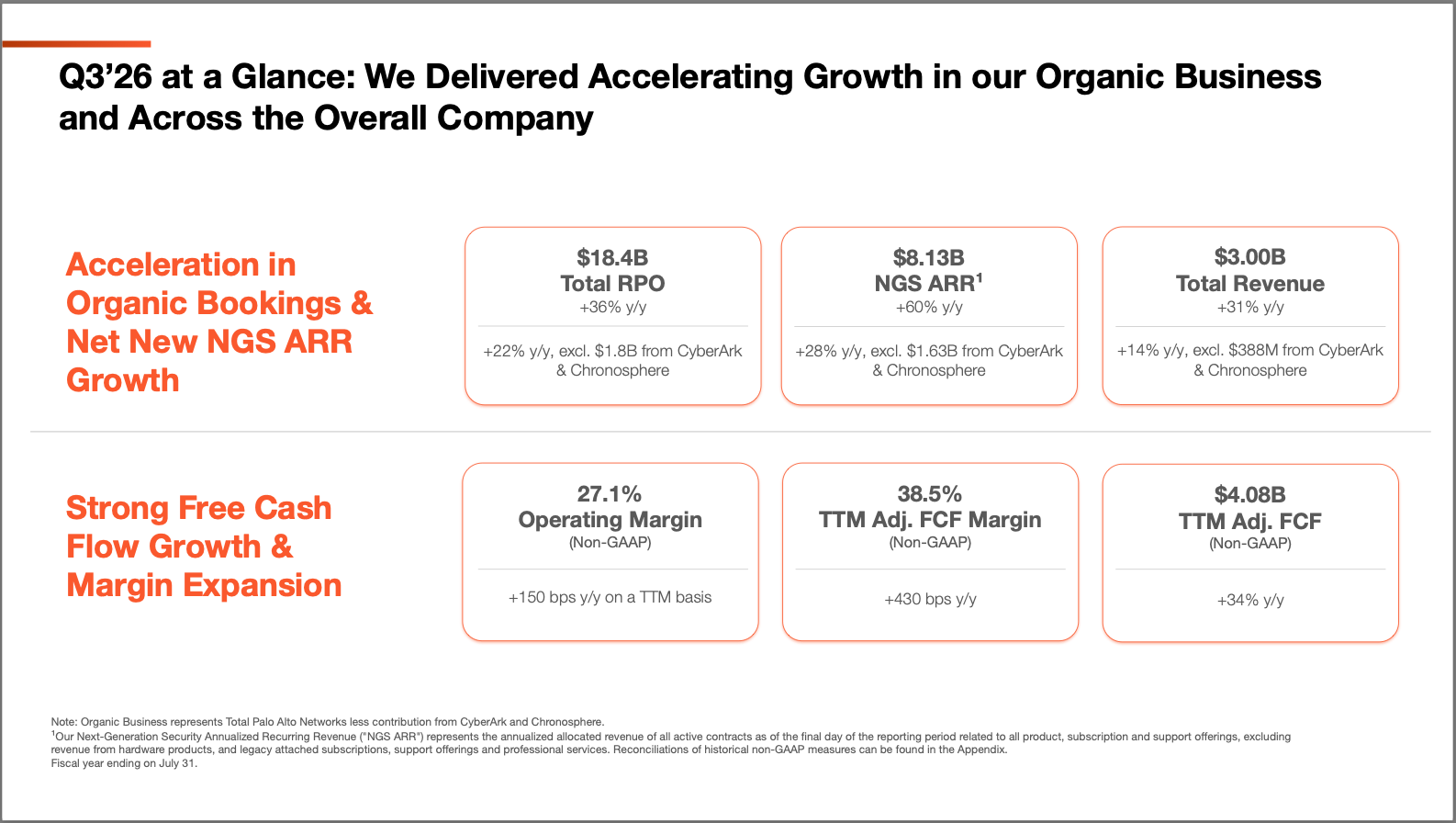

For all the noise around the print — a record quarter, every guided metric beaten, full-year guidance raised across the board, and yet a ~5% dip in the stock — the story at Palo Alto Networks (PANW) is one of a company that knows exactly where it is going and is methodically getting on with it. Revenue grew 31% to $3.0B and NGS ARR 60% to $8.13B. Strip out CyberArk and Chronosphere and the organic engine still grew NGS ARR 28% — right at the ~30% compounding pace required to hit the $20B-by-FY2030 target we have been tracking. Steady as she goes.

There are, in effect, four things management is steering at once, and Q3 showed progress on all of them. First, integrating and building new product capability from the CyberArk and Chronosphere acquisitions — and, just as importantly, making them succeed: both are running ahead of plan, with CyberArk's integration 3-6 months ahead of plan and ARR growth of 27%. Second, compounding NGS ARR toward that 2030 ambition, with platformization (2,280 customers, 120% net retention) the stated engine. Third, meeting the opportunity AI is opening up — Prisma AIRS is already the fastest-scaling product in the company's history, and Arora's data-as-fuel thesis is converting AI threat-urgency into bookings. And fourth, working margins and SBC (stock based compensation) back toward pre-acquisition levels over the next 12-18 months.

The contrast with the rest of our coverage universe is stark. As we noted in our Zscaler Q3 earnings review, ZS is guiding FY27 to just 16-17% growth amid sales-leadership turnover while NET is eliminating 20% of its workforce. PANW, meanwhile, is the one large-cap name turning the agentic-AI narrative into accelerating bookings, with an acquisition machine that — unlike ZS's Red Canary — is adding to growth rather than dragging on it.

The catch, if there is one, is price. At 68x EV/EBITDA - a higher multiple than AVGO or NVDA, and both growing much faster - Palo Alto stock commands a premium valuation and will need to deliver fully on its potential to justify these multiples. Quality has never been the question; the only question is whether valuation leaves room for future gains.

Here are the headlines.

Analyst Insights

NOTE: PANW's earnings call transcripts contain many valuable insights on product performance, industry dynamics and the future direction of cybersecurity, and much more than the earnings presentation conveys. For anyone interested in cybersecurity stocks generally, and PANW in particular, it is a 'must read'. This quarter's can be reached here.

Growth

- Q3 revenue of $3.0B grew 31% yoy, beating the $2.94B guide and included $388M from CyberArk and Chronosphere. Stripped out, organic revenue grew 14% — in line with the mid-teens organic run-rate, the headline acceleration being acquisition-driven. Product ($594M) and services ($2.4B) both grew 31%.