Natural Gas Securities Positioning

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Analysis by Alex King, CEO, Cestrian Capital Research, Inc + Claude CoWork

Yesterday I walked through the securities positioning setup in oil. If you missed it you can read it here.

Today, a look at positioning in natural gas.

In essence: the crowded-short trade is less intense than the oil market, and the divergence with physical product is also less marked. I don’t know if long plays in oil will win out, but I would say conditions for that are more convincing than long plays in natural gas at the present moment.

As a reminder, I am no oil and gas expert. What interests me in oil is the night-and-day comparison between physical oil (expensive and in short supply if you want rapid delivery) and financial oil (cheap). I am therefore curious about conditions in natural gas securities. Understanding securities positioning in each market is a great backdrop for price and volume analysis.

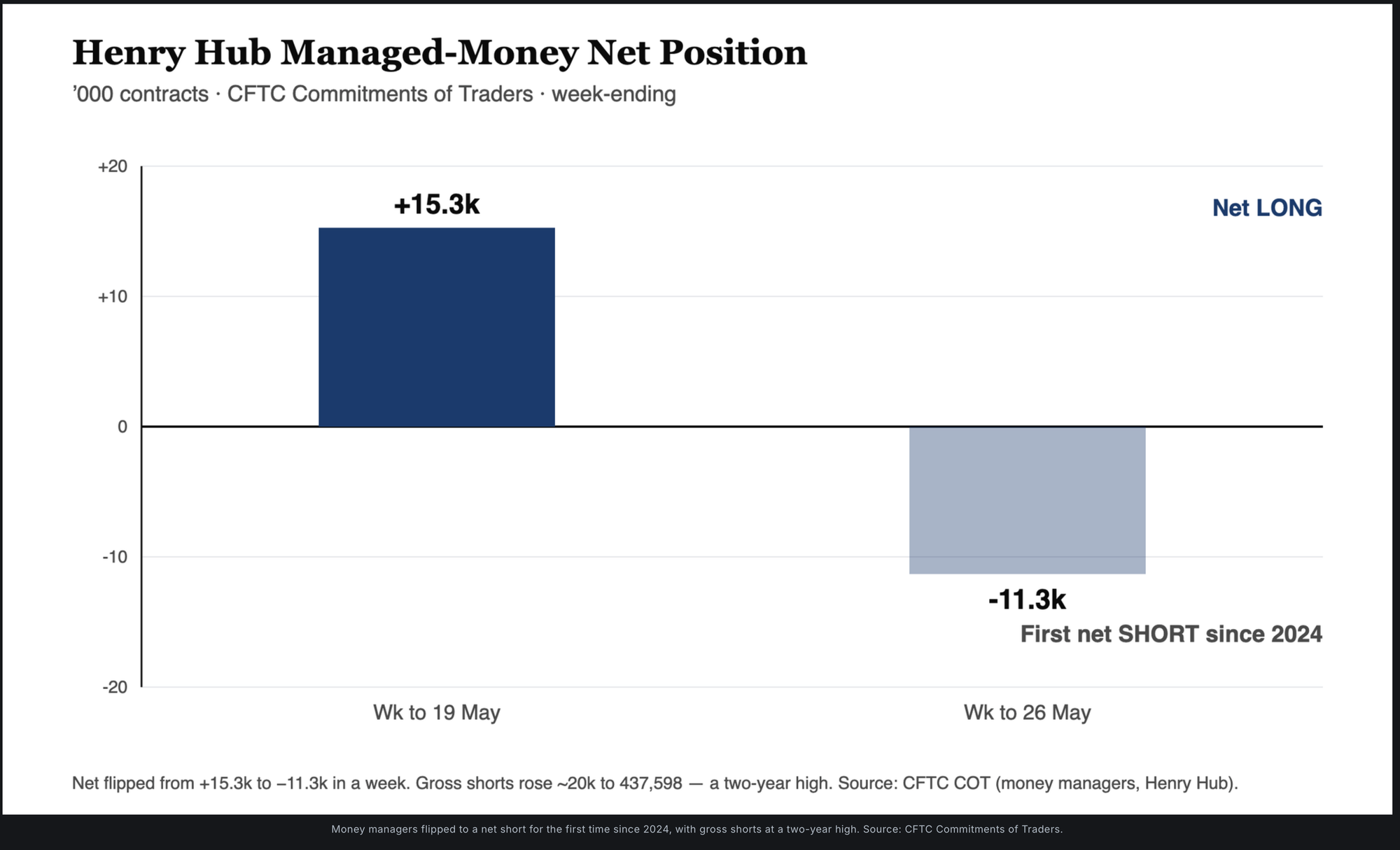

Positioning Is A Little Bearish

As at the end of May, money managers moved to a net-short position of 11,316 contracts in Henry Hub futures — the first net-short stance since 2024 — reversing a net-long position of 15,270 contracts the week before. That is a meaningful swing in sentiment in a single week. Underneath the net figure, the gross short position jumped by nearly 20,000 contracts to 437,598, the highest level in more than two years. So while the net short is still modest, the gross short base is now large and crowded. This is viewed as a reaction to oversupply in US markets.

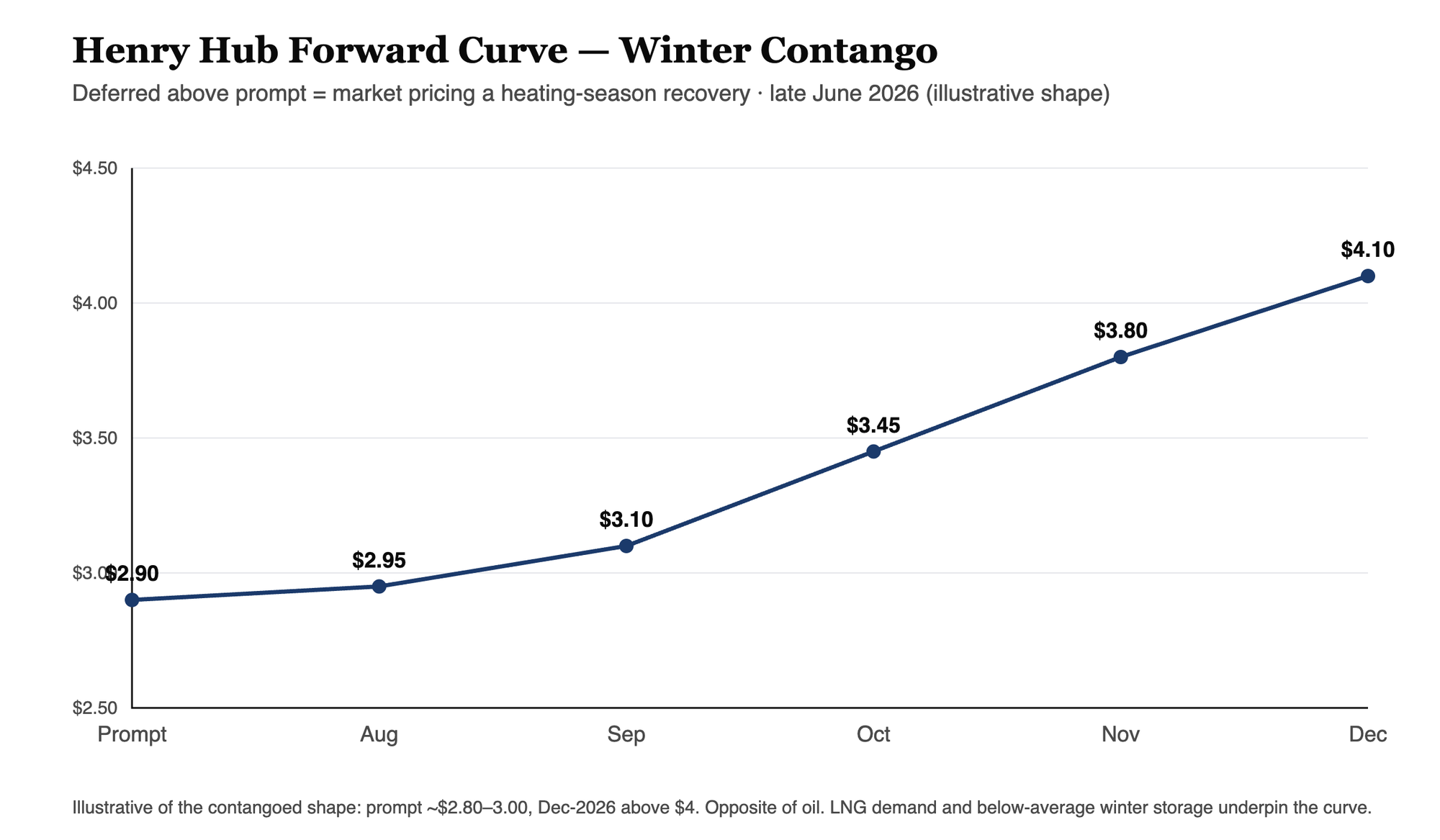

Seasonality Applies

Gas for delivery in the winter is priced more highly than gas for delivery in the summer. It doesn’t take a fluid dynamics scientist to work out why.

There is also a question around U.S. gas exports. If the ability of Gulf countries to export has been diminished by the war in Iran - here I have Qatar in mind of course, which is second only to the U.S. in natural gas exports - then overseas demand for U.S. gas will rise and take price upwards with it.

This I think is the most likely trigger for any unexpected rally in gas futures, and it’s very difficult to get a fix on the probability of this at present.

Cestrian Capital Research, Inc — 25 June 2026

DISCLOSURE: I am long $EQT.