ASML Q1 FY12/2025 Earnings Analysis

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

By JamsODonnell

Summary:

- Demand for ASML photolithography tools is high and so far unaffected by trade restrictions

- Management guide for revenue growth in 2025 and 2026

- Uncertainty is high, margins will probably shrink

- Stock might still go lower. Rating: Do Nothing.

ASML is the first semi cap equipment supplier to report after the tentative establishment of a new tariff scheme in the US, so much of the Q&A circled around the "how is this going to affect the industry" question. At times the listener might have had the feeling the call was turning into a group therapy session for US analysts. As far as the ASML business is concerned, the message is quite clear:

- They see no impact in net bookings so far.

- Their customers are sticking to their plans so far, i.e. 2025 and 2026 will be growth years.

- Management is sticking to the 2024-issued guidance, which is €44-60 billion TTM revenue by 2030.

- All of this with the caveat that nobody really knows how tariffs will affect the macro environment.

- As for next quarter, they have adjusted guidance to reflect potentially lower margins due to the uncertainty.

My understanding is that demand for the big semi cap equipment suppliers is unchanged, high, and quite inelastic. Among other things, orders are tied to the construction timelines of the fabs, i.e. chip manufacturers can't stock up on gigantic photolithography tools this quarter just in case tariffs get really bad - they have no place to put those beasts in, if the fab isn't ready.

Short-term, ASML expects the extra costs introduced by tariffs to be spread across the supply chain. Longer term, the question is really how much the new world trade order will impact GDPs, hence demand for semiconductors. Some of that potential decrease will be mitigated by the inherent inefficiency of having to duplicate fabs in different geographic regions. So far, nobody knows.

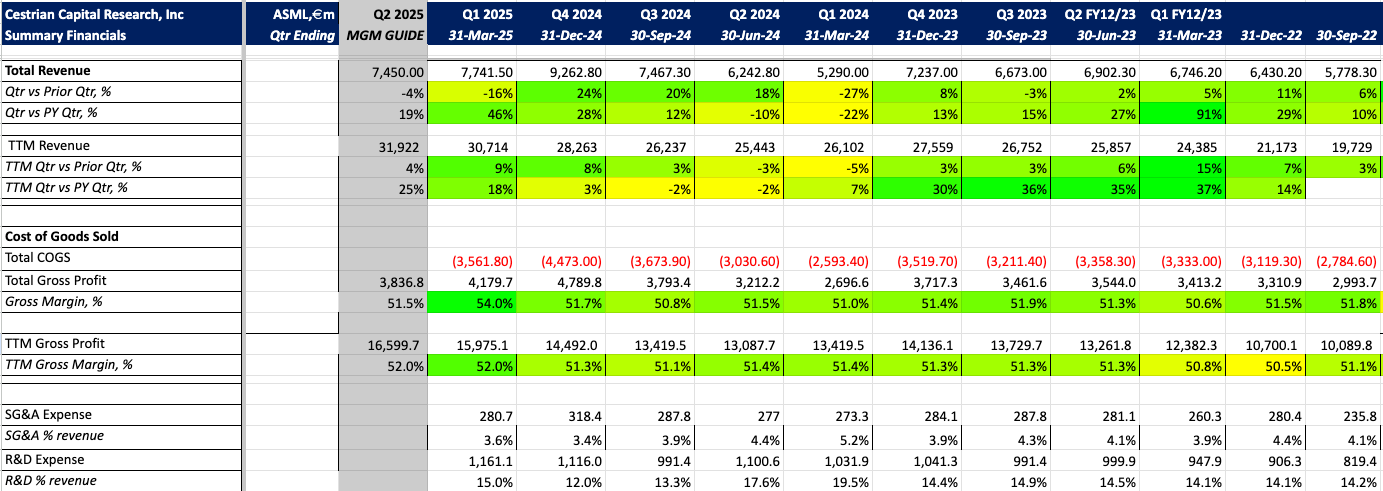

Here the numbers:

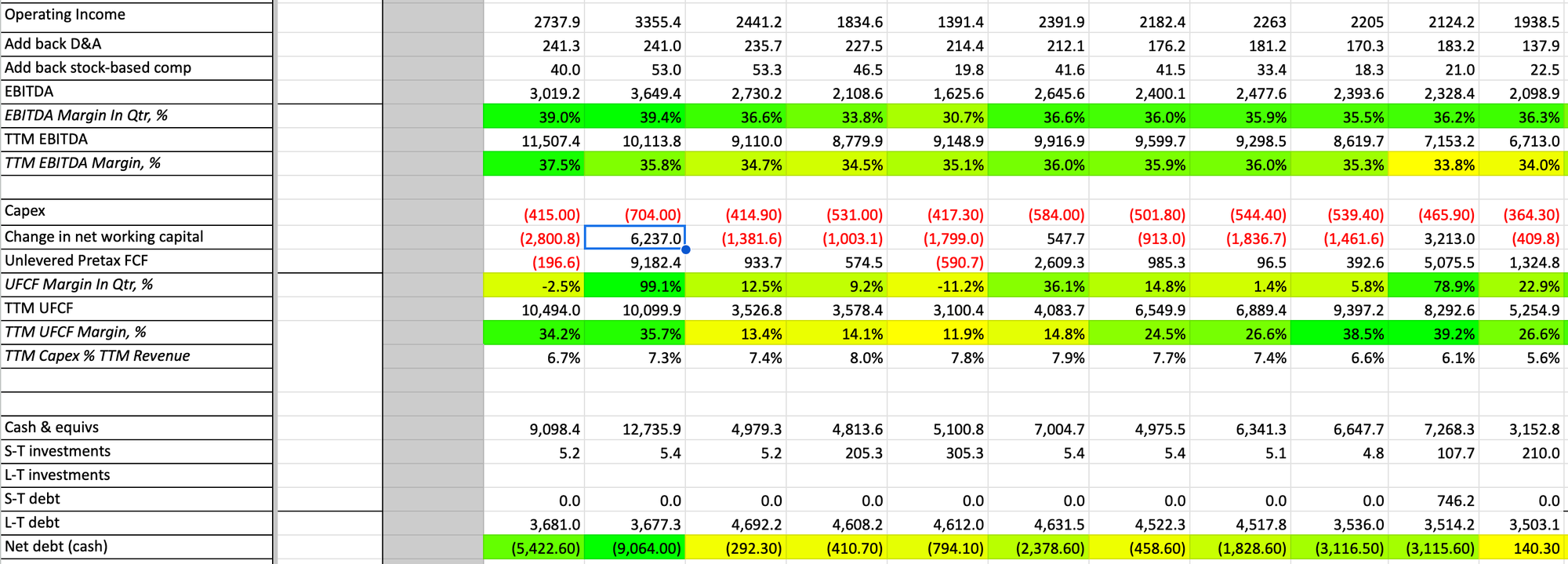

As my kids would say, ASML net system bookings be like:

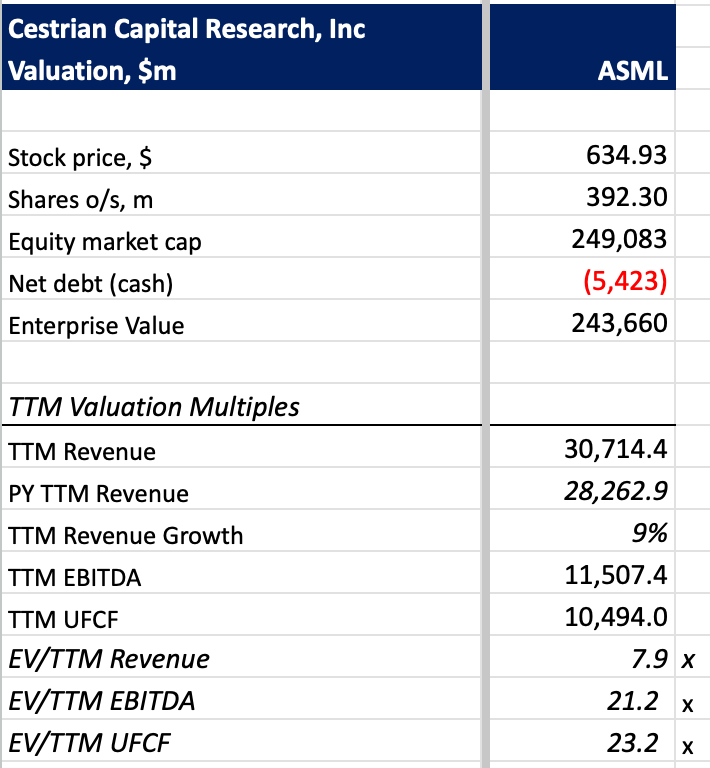

Valuation if that matters:

Technical analysis

https://share.trendspider.com/chart/ASML/76369l5z1e9

ASML's chart has always been more difficult to decipher. I have redrawn it now with the W1 starting in late 2018. In this scenario, the W5 peaked in July 2024 at the 100% extension of the W3. I see at least two scenarios for the a-b-c correction we're potentially in. 1) Optimistic view, the a wave bottomed in July 2024 and price has now reached a potential bottoming area (c = a in price). 2) Less optimistic, dashed-dotted lines, the (a) wave bottomed in Nov 2024, then the (c = a) price level is in the low $300s.

I'm not highlighting accumulate zones here because really nobody knows what's going to happen.

Rating: Do Nothing.

Disclaimer: I have no position in ASML and I am not planning to start one in the next 72 hours.