Salesforce $CRM Q1 FY1/27 Earnings Review (The Cestrian Circle Newsletter - NO PAYWALL)

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Read our full disclaimer, here.

Analysis by Alex King, CEO, Cestrian Capital Research, Inc.

We’re a Salesforce customer, specifically for Slack. We use the enterprise version which is fearsomely expensive; this is because we’re an SEC-regulated business and we want all our Inner Circle subscriber communications - trade alerts, ratings changes, algo signals, chat - to be (i) always available - Slack’s uptime is incredible - and (ii) fully compliant with all message retention and retrieval policies that regulators may adopt from time to time. You can leave your regular Furu Discord Server at the door, thankyou.

Salesforce, whilst always polite and engaging, are extremely tough commercially to deal with. They miss no opportunity to jam through a price rise, prevent you from optimizing your spend, billing you for support or implementation or explaining to you why you can’t do something yourself and need to pay one of their partners to help you. And since they are a behemoth and we are not, they don’t care what we have to say about any of this stuff. Buy it, don’t buy it, is probably what they think of our attempts to manage our spend with them. Customer-friendly they are not, in contrast to their early days (being old I remember this well) when they would literally fall over themselves to get you to use the CRM product. Generally speaking we can see this as characteristic of a mature business where revenue growth is dependent as much on customer lock-in and price rises as it is on new-name contracts. As a customer it is no fun to deal with, I can tell you.

The golden rule of investing and trading is: forget your own opinions, experiences, any attempt to map the real world of the company to the stock. Because that is just likely to blind you to a cool and rational analysis of the stock’s trajectory.

And in that light I am here to tell you that we move now to Accumulate rating on $CRM stock. The technical setup looks compelling - by which I mean a sound upside opportunity with the stock in a place where a stop can be placed at a sensible level, not too far below spot so that if it trips you aren’t hurt too badly. Fundamentals are good, solid, improving and valuation multiples are rather low as a function of the company’s growth and margin profile. Finally the company has executed a giant buyback (the share count fell by around 10% recently) which tells you that the company at least thinks that a good use of cash is deploying it into their own stock.

The context of course is that money is now rolling into software stocks, having shunned them for about nine months now. This sector rotation should act as something of a tailwind for the stock too.

Let’s start with the most important part - the chart - that tells us what major market participants think of the stock.

$CRM Stock Chart

You can open a full page version of this chart, here.

Volume x price has picked up in the $165-$200 range; the stock is currently at $191. Our second-derivative indicator believes the stock is in a bottoming phase on the weekly.

I think a stop can be placed below that $165 level - let’s say you wanted to stop out at $160 (below the recent lows), that’s a 16% drop from here. You may choose to use a trailing stop which will follow the stock upwards if it runs. As regards position sizing, my preferred method is to consider how much capital I am prepared to lose on each trade - for me here I would accept a loss of 0.5 units of capital, I will use a 16% trailing stop at inception, so my initial position size would be 0.5/0.16 =3.125 unit commitment. You will have your own methods of course. We can discuss in real time in Slack if you’re an Inner Circle member.

The stock is likely to encounter some difficulty in the $220 zip code which is where the 200-day SMA lives. This is a standard battleground between buyers and sellers. Personally I will probably hold the stock if it tries to break up and through, but a lower risk approach here is to wait to see if that that 200-day SMA to be defeated, and if so, to buy the stock above that level with a stop below it.

Conversely if and when the stock gets up and over the 200-day the upside becomes easier, as buy programs are likely to apply if the stock does get over that level.

$CRM Financial Fundamentals

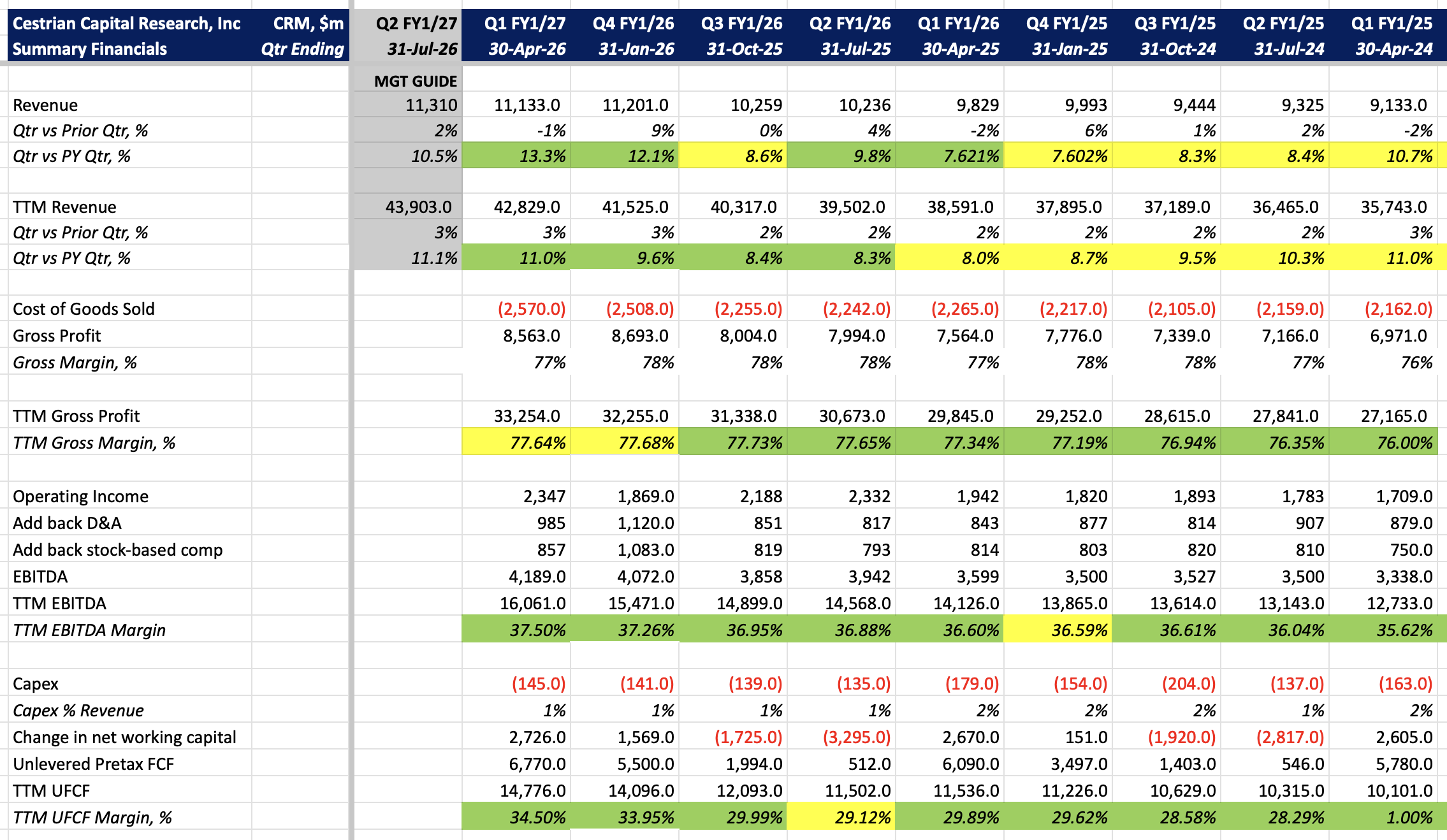

The numbers are good. Not stellar, but good. It’s OK that they aren’t stellar because (i) sentiment is so bad around the “AI is killing software” narrative that these numbers look good in that context and (ii) the valuation multiples are very low in the context of this market.

Revenue growth is accelerating and cashflow margins are rising.

In addition, the order book (RPO) looks very solid and its growth vs. prior year is accelerating.

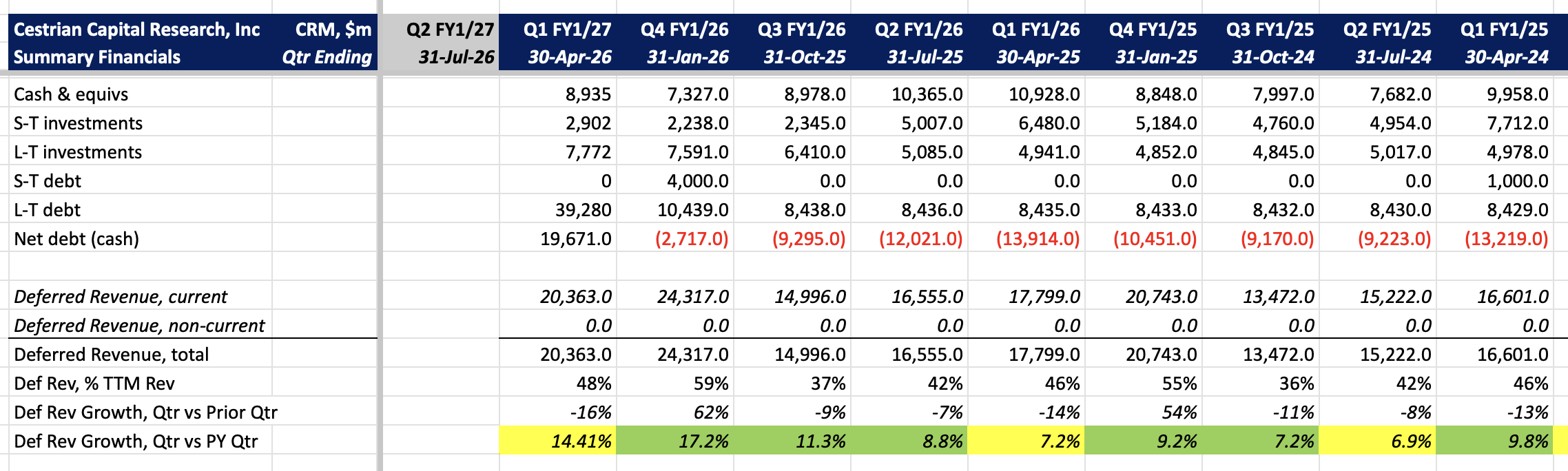

The balance sheet is now levered as a result of the debt-funded buyback campaign, but the leverage is very light at just 1.2x TTM EBITDA and the company’s gross cash balances remain large. Deferred revenue (the prepaid portion of RPO) is seeing slower growth - that’s something to watch.

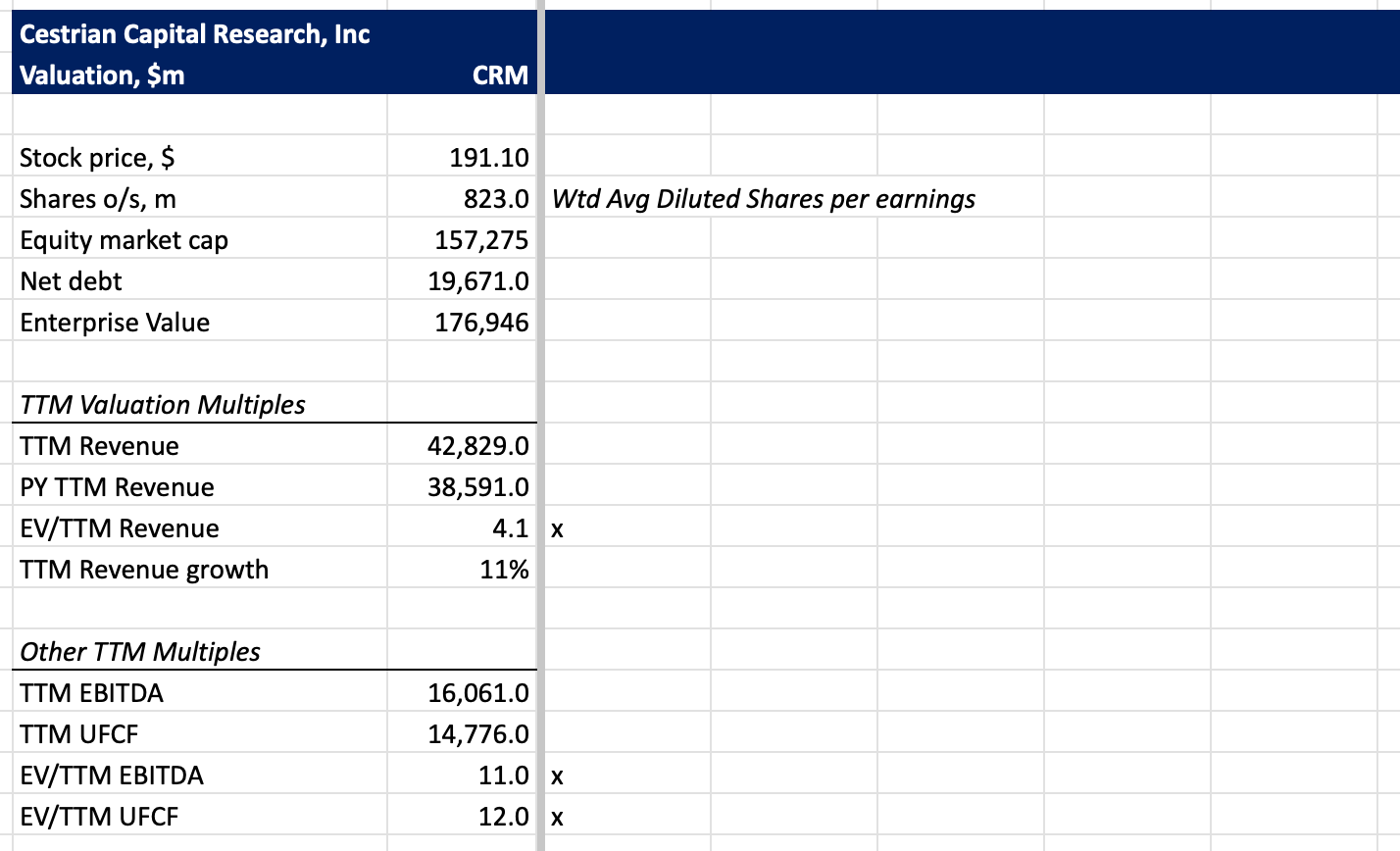

$CRM Valuation Multiples

12x TTM cashflow is your parents’ valuation for an 11% growth / 35% cashflow margin / 1.2x TTM EBITDA levered business. It really isn’t expensive.

Final Word

Thanks as always for reading out work. Any questions, reach out in the comments to this article.

Cestrian Capital Research, Inc - 30 May 2026.

DISCLOSURE: Cestrian Capital Research, Inc staff personal accounts hold long positions in $CRM and plan to add further positions on Monday 1 June.