Join Jay’s Options - For A Statistical Edge

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

All About Jay’s Options

by Jay Urbain, Ph.D

Our Mission

This service stems from my own desire for evidence based, data driven methods to help me generate income from options in any kind of market. I struggled to find this information and so I developed my own system using my experience in computer science and data analysis. I felt strongly that others could benefit from my experience - this service is the result of that desire to help others.

How We Do It

We apply data science methods to options and other market data to identify where we have a statistical or positional edge. Unlike many trading indicators, option data is forward looking. It captures the collective wisdom and sentiment of traders willing to put down hard earned cash to express their belief. We then layer on knowledge of dealer positioning (hedging flows), technical analysis, and models of volatility and market cycles to identify specific high probability strategies.

What You Get As A Subscriber

- Daily charts, reports, and narrative of integrating data and models of volatility, option dealer positioning, and technical analysis to inform option strategy selection and strike price placement.

- Daily option trade ideas.

- Real-time option trade model portfolio of the option strategies we use in the service.

- Articles and presentations on trading strategies including specific strategies for placing and managing trades.

- Ongoing research, backtesting and live experimentation of new strategies.

- Membership of a superb, smart and collaborative community available 24/7 in our real-time chat environment.

Join Us!

We offer this service with two pricing tiers.

If you’re an investment professional - as defined in our terms and conditions, here, then choose “Jay's Options - Pro Edition”. The terms of this subscription enable you to share the model outputs with anyone in your own firm. You'll pay $3999/yr, a 33% discount on the monthly subscription of $499/mo.

If you’re not an investment professional under our terms and conditions, choose “Jay's Options - Independent Investor”. This subscription is for individual use only; model outputs are not permitted to be shared. The annual subscription is $1999/yr, a 32% discount on the monthly alternative of $249/mo.

Go Deeper

Want the deep dive? Here's the deep dive.

Introduction:

My background is computer science. Many years as a professor, scientist, and consultant. My basic area is applied data science and machine learning. Most of my work is in the medical field, so the work I do and the models I create need to be statistically sound and data driven. I try to bring the same rigor to analyzing option and market data to identify metrics, strategies and opportunities where we can have a statistical or positional edge trading stocks and options. With this service, I hope to share this information and create a collaborative and open learning environment where our strategies and methods are continually improved and adapted to new market regimes.

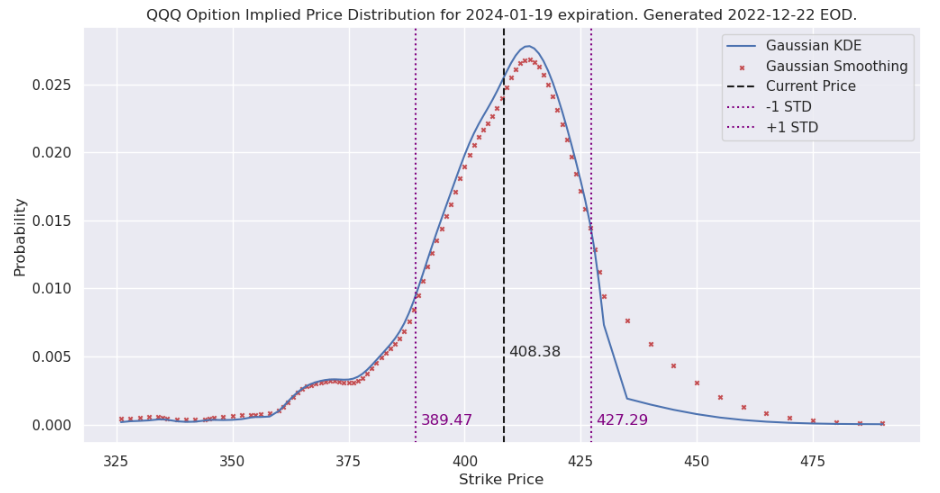

Implied Distribution

Unlike many trading indicators, option pricing, volatility, and positioning is forward looking. It captures the collective wisdom and sentiment of traders willing to put down hard earned cash to express their belief. Option pricing models are not perfect, but they’re theoretically sound. For example, we can generate the implied distribution of stock prices for any given expiration date (Fig. 1). The distribution indicates that there is a 68% chance the stock price will be between $389.47 and $427.29 (+/- 1 standard deviation) by the expiration date. I have back-tested this on several indices and the number is close to 70-71% (likely due to the variance risk premium, more later). This is a statistical edge you can use to help build a trading strategy along with technical indicators and fundamentals. In fact, regularly selling 30-DTE (days to expiration) Iron Condors with short strikes outside this range is a reliable income strategy. The more accurately we can predict this range, the more precisely we can set strike prices, and the more profitable our strategies become.

Figure 1. Implied Distribution of QQQ

Variance Risk Premium

The variance risk premium manifests as a long-term difference between option-implied and expected realized asset price volatility. It compensates investors for taking short volatility risk, which typically comes with a positive correlation with the equity market and occasional outsized drawdowns. And historical data shows that perceived uncertainty in the market (IV) tends to overstate the realized underlying price move more often than theory suggests. To capture this, we have created custom screens to identify candidate trades where option premium is selling for greater than the expected realized volatility and when the underlying asset has an identifiable trend.

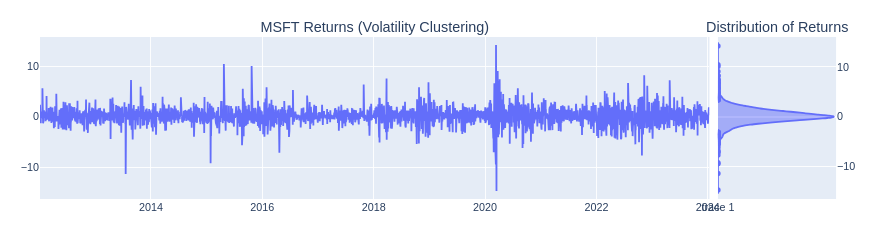

Realized volatility prediction

Here we show how volatility clusters and mean reverts. Overtime, this is predictable. The log returns of a stock or index generates a near normal distribution which we can use to identify the likely expected range of a stock at any point in time.

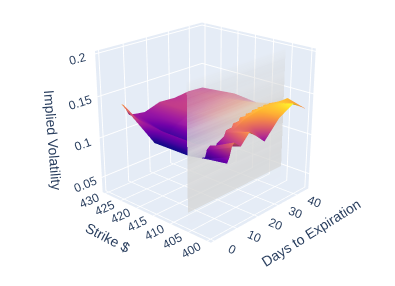

Fig. 2 shows a QQQ option implied volatility (IV) surface. The values for IV are output from an option pricing model given the price of an option for a particular strike price, the expiration, the risk free rate, and dividends if any. We can use these values to predict the expected range of the underlying. And we do, however, option pricing models typically do not capture liquidity (supply/demand), exogenous events like earnings, Fed speak, and company announcements.

Fig. 2. QQQ 1/9/2024 Expiration Put Options Volatility Surface

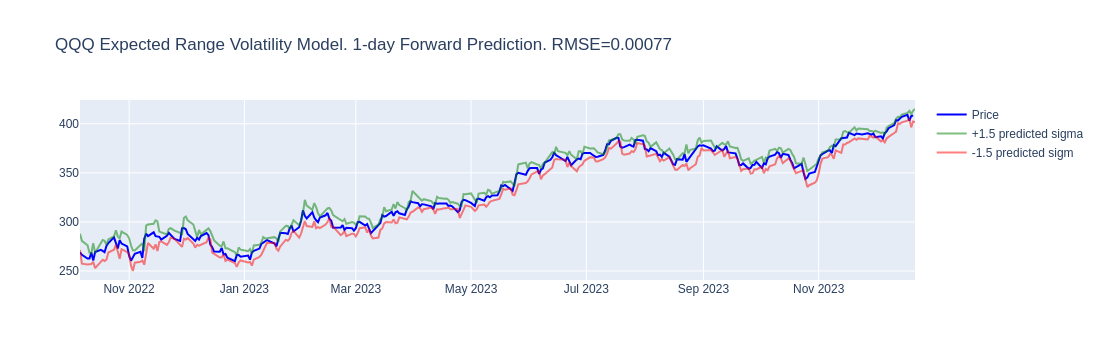

To address this, we’ve built several machine learning models that predict future volatility, ATR (average true range), and returns. With these volatility models we can more accurately predict the short term expected range of the underlying. And more accurately identifying the expected range is key to successful trading. We can also use these models to compare our model’s predicted volatility to the implied volatility of any option contract. This allows us to better identify options that are underpriced, over priced, or fairly priced. This consequently drives the type of option strategy we would use, i.e., short volatility, long volatility, or neutral. Concretely, this provides us with an additional statistical edge.

Most traders and websites use IV Rank or IV Percentile, however these metrics tell you if an option is historically underpriced or overpriced. It doesn’t tell you if it is correctly priced for the current market regime.

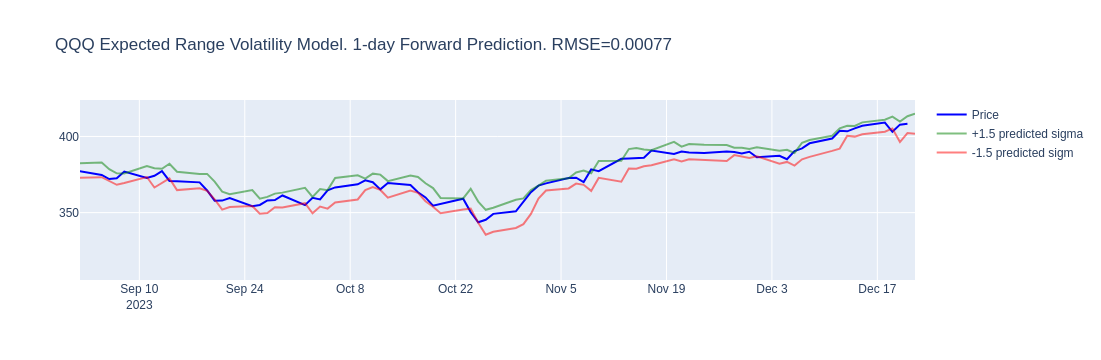

Below are plots representing our 1-day forward realized volatility prediction. The model has been very accurate. If we use a 1.5 the predicted reliability, the model has accuracy that exceeds 96%.

Fig 3. Expected range volatility model

Fig 4. Expected range volatility model - zoom view

Market Maker Option Positioning

Delta-gamma hedging is an options strategy that combines both delta and gamma hedges to mitigate the risk of changes in the underlying asset as the underlying asset moves. Delta tells a trader how much an option's price is expected to change with a one-dollar change in the underlying price. Gamma refers to the rate of change of an option's delta with respect to the change in the price of an underlying stock’s price. Essentially, gamma reflects the fractional amount of change in the amount of hedging required to maintain a delta neutral hedging strategy.

Market makers use gamma, vanna (change in an options price with respect to the change in volatility) and charm (change in an options price with respect to an options expiration date) to maintain a delta neutral position. Market makers make money through the bid-ask spread and want to avoid any directional risk. Over the last several years, there’s been a dramatic increase in option trading and structured products. Structured products can be large mutual funds selling call options to help pay for downside put option protection. These large option trades can create large hedging flows from market makers who must buy or sell the equivalent of the underlying to stay delta neutral (directionaly neutral). These hedging flows can create support or resistance, a pinning effect, or an acceleration (gamma squeeze) at heavily optioned strike prices. By calculating the gamma, vanna, and charm weighted open interest exposure at each strike price, we can use these strike prices in our trading strategy. Fig. 4 shows the daily open interest weighted gamma, vanna, charm, and delta exposure for QQQ. Option strike prices with large hedging exposure are clearly visible.

Fig. 5. QQQ Gamma, Vanna, Charm, and Delta weighted open interest

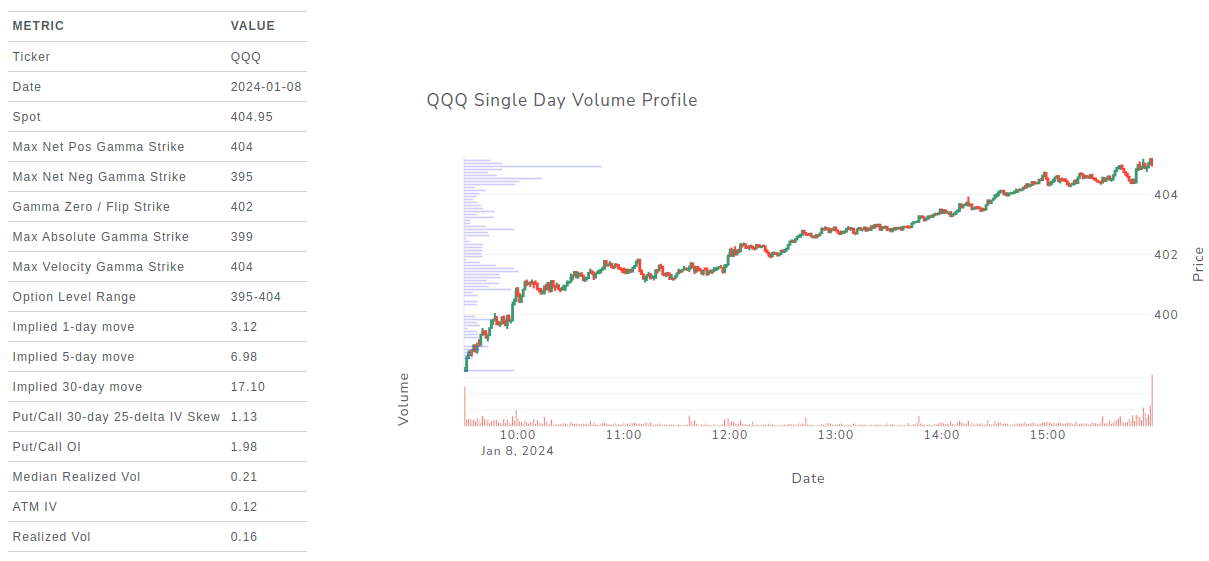

Integrating statistical and positional indicators with other technical indicators increases the utility of these methods. Fig 5 shows net gamma weighted open interest exposure as a bar chart (net calls are green, net puts are red), volume a price profile as a blue bar chart, and expected range as dashed lines over the price action for QQQ. The idea is to provide a quick view to identify confluences between indicators.

Fig. 6. Integrated view

Market maker hedging exposure can significantly affect stock prices on key monthly and quarterly options expiration dates. Fig. 6 below shows options expirations by date.

Fig. 7. Options Expiration

Fig. 8. Shows a daily tabular summary of these metrics.

References (incomplete):

Historical Performance of Put-Writing Strategies (2019), https://cdn.cboe.com/resources/education/research_publications/PutWriteCBOE19_v14_by_Prof_Oleg_Bondarenko_as_of_June_14.pdf

Generating Income and Managing Risk: Cash-Secured Put Writing in a Low Equity Return Environment, Stephen Solaka, CBOE. (2023)