Salesforce (CRM) Q4 FY1/24 Earnings Review

- Salesforce is growing old mostly gracefully, but whilst revenue growth is gently slowing, cashflow margins are below best in class for a mature software company.

- We rate at Hold on technicals; valuation is a little pricey but nothing to trigger a buy or a sell decision in and of itself.

- Read on - the detail matters in this note.

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Old Software Companies Never Die

by Alex King

Salesforce (CRM), once the enfant terrible of enterprise software, is now sat comfortably in the old folks’ home with pipe, slippers, and a “dang those yahoo youngsters” take on life. It has, in short, become its alma mater, Oracle (ORCL). Although without the killer cashflow margins.

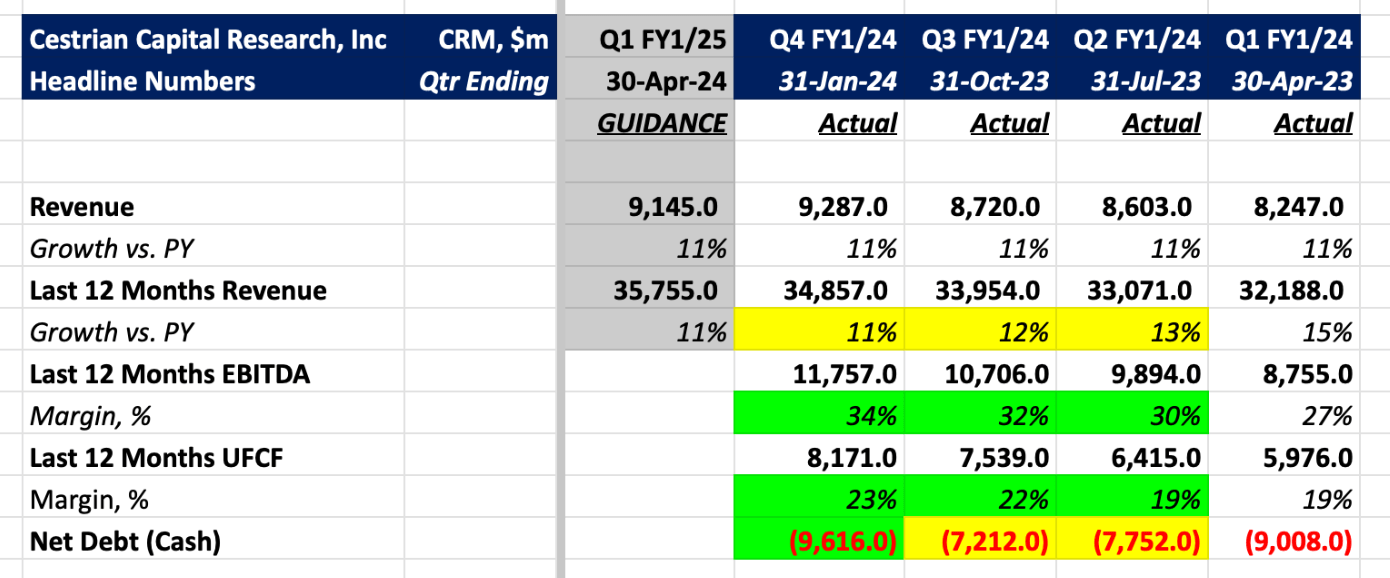

Here’s the headline numbers.

In short:

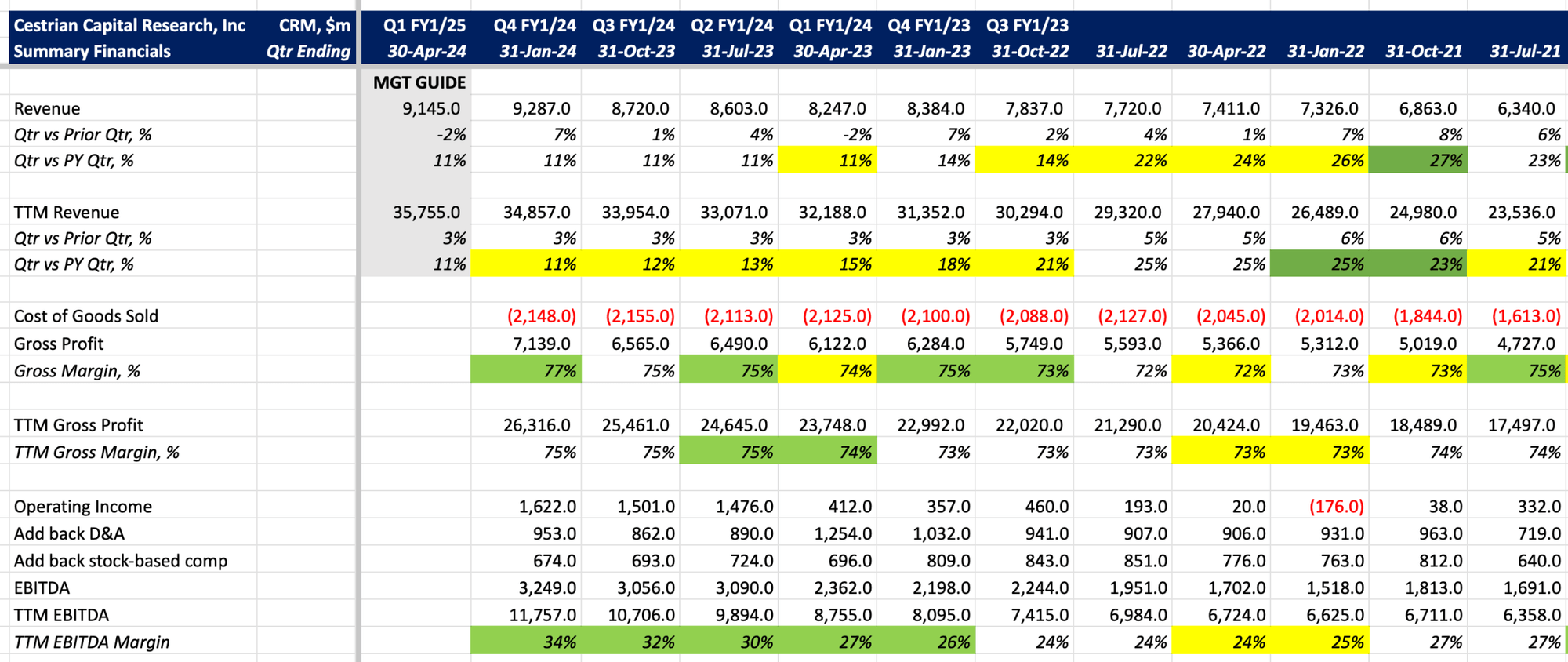

- Revenue growth remains at 11% vs PY this quarter … the same growth rate for the last three quarters … and the guide for next quarter is … you guessed it … 11%. That is an unusual level of consistency.

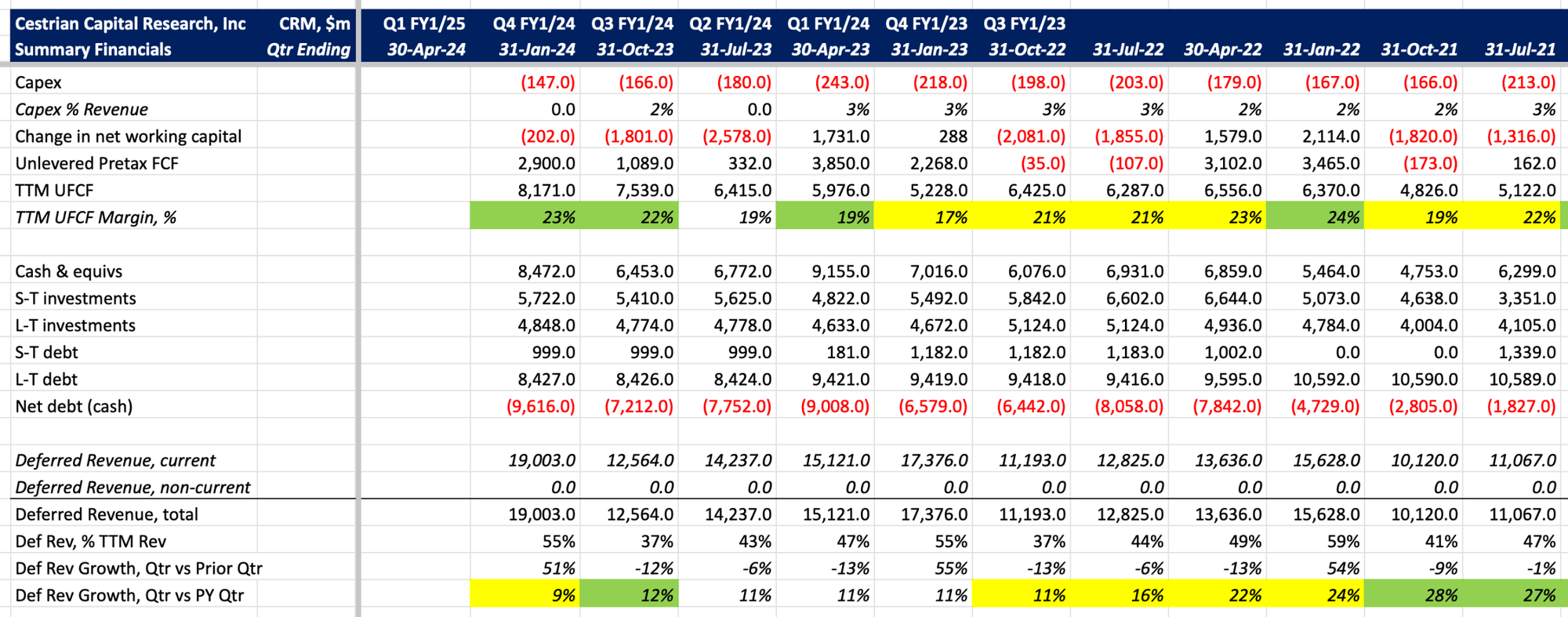

- EBITDA and cashflow margins are climbing nicely, but note the meaningful gap between them. For me this means I tend to disregard EBITDA and focus on cashflow; and those cashflow margins are rather low for the business model. Grandpa Larry will give you >40%, come rain or shine.

- The balance sheet is safe as houses, with almost $10bn of net cash now (if you deduct the value of their long-term equity investments, a more cautious measure, you can say there is around $6bn net cash).

Let's turn to the valuation analysis, stock price outlook, our rating and more detailed financials.

Read on!

Get our 🎥 content, click here and subscribe.

Not a paying member? Subscribe for fundamental and technical analyses of 40+ stocks. Hit the button below now!

Enjoying our work? 🌟 Help us grow by sharing our newsletter with your social network. 🚀

Valuation

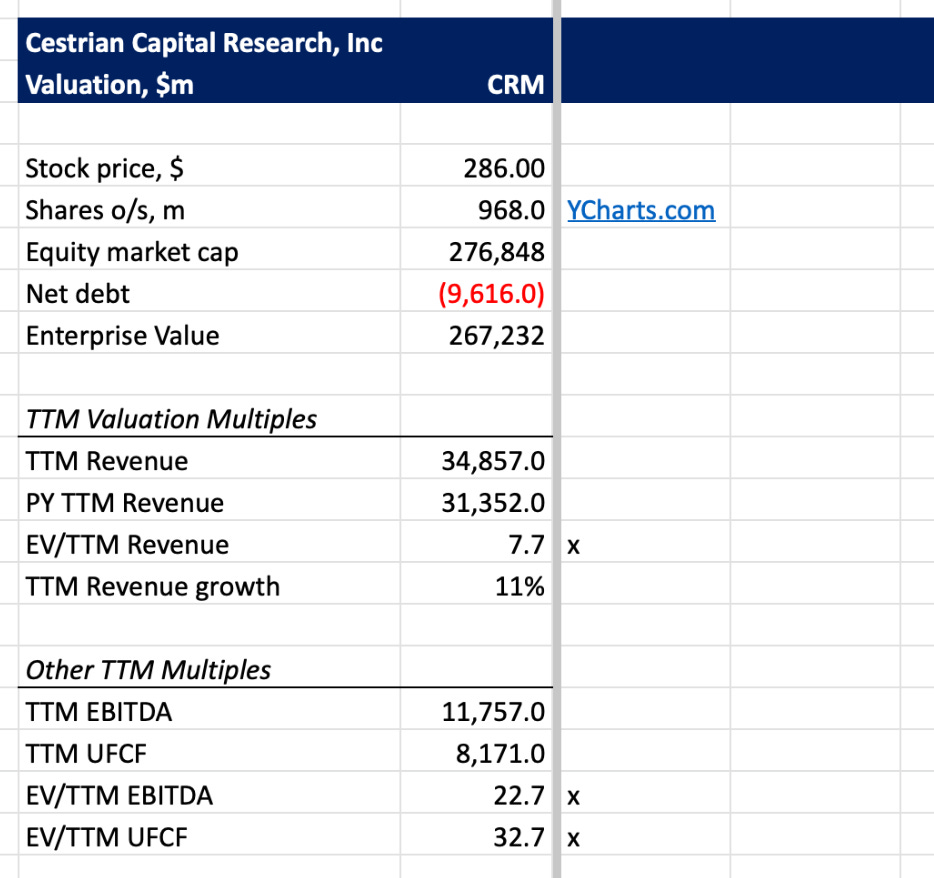

The stock is a little pricey in my view - nothing silly, but if I was paying 33x cashflow for this thing I would hope to see a more aggressive restructuring plan in place so that cashflow growth would be faster than is currently the case. The current valuation though is not a reason to buy or sell in my view - it’s not close to extreme lows or highs.

Technical Analysis

CRM stock was truly brutalized in 2022, overly so in my opinion. The stock bottomed in December 2022, just a few dollars above its late 2018 low. The recovery was equally sharp. We rated CRM at Accumulate between $138-166/share, reflecting the concentration of institutional buying at the time; the stock is now sat at around $308 after a modest selloff on earnings. So, an opportunity to have doubled your money in not much more than a year, in a stable software business with a solid balance sheet. Not too shabby.

Here's how we see the stock longer term. You can open a full page version of this chart, here.

On a shorter term basis, the stock has hit resistance right around the 100% extension of the prior Wave 1. That’s a modest extension at which to sell off in a bull market, so more upwards movement may be expected. I would be surprised if the stock climbed past around $374 (the 1.618 extension of the prior Wave 1) before a material retracement, but at the moment most surprises are to the upside, so as always one should let price say what price is and not try to second guess.

You can open a full page version of our shorter term chart, here.

Stock Rating

Formally speaking, we rate the name at Hold, because if the market keeps moving up - which we think it will, see our long-term take on markets here - then most likely CRM can tag along, per our charts above.

Personally, I hold no position in the name, because I can think of other places I would prefer to have my capital at work. On fundamentals, the company is neither fish nor fowl; not high growth, and not high margin either. As growth drops below 10%, which it likely will here in due course, a well-managed mature software business ought to be clicking in 35-50% unlevered pretax free cashflow margins. CRM is achieving only 23% TTM UFCF, which says that there is a lot of wasted spending in the business. Spending is fine if it ramps up the growth rate, but if growth doesn’t respond to spending, then at this stage of a company’s lifecycle it should be cut, in my view. There is something of a restructuring program afoot at Salesforce but not, as far as I am aware, one that will deliver Oracle- or Microsoft-style cashflow margins.

Let’s take a look at the detailed numbers.

Fundamental Analysis

Here's our detailed take on Salesforce fundamentals.

Any questions, reach out in chat!

Cestrian Capital Research, Inc - 29 February 2024.